Executive Summary

Act III of COVID: Navigating the Crosscurrents of Post-Inflation

2022 ushered in Act III of the market’s latest transitionary period: The Post-Inflation Era. Since 2008, the US economy functioned with remarkably low inflation and interest rates. As the cost of capital went lower and lower during the decade, valuations steadily rose. Between 2010 and 2020, the NASDAQ experienced a 17.1% annual growth rate, with no small share of the growth a result of expanding valuation multiples in addition to earnings growth. An entire generation knows no other environment than cheap capital and climbing valuations. The story began to change in late 2021 as steep inflation took center stage thanks to a near-perfect confluence of excess liquidity, demand acceleration, and supply constraints. As inflation rates rapidly accelerated from 1% to over 9%, and market sentiment on inflation shifted from “transient” to a feeling of being “entrenched”, the market extravaganza that was 2020-2021 came to a screeching halt after a period of extraordinary gains.

Act I: Pre-COVID (Pre-2020)

Act II: Post-COVID (2020 – 2021)

Act III: Post-Inflation (2022 – ?)

We leveraged our experience executing transactions, extensive network, and market analysis from our 16-year history of advising and selectively investing across the ever-evolving Health IT and Digital Health sectors to gather key market information. We’ve bifurcated this market information between hard data (facts) and the accumulation of our anecdotal experience (observations). Beginning with the facts, the data shows that while it certainly has felt as if we’ve been on a sharp downturn when taken within the context of where we were before the pandemic, valuations, investment value, and M&A volume continue to be at healthy levels, though the downward trajectory is undeniable.

HGP Facts and Analytics

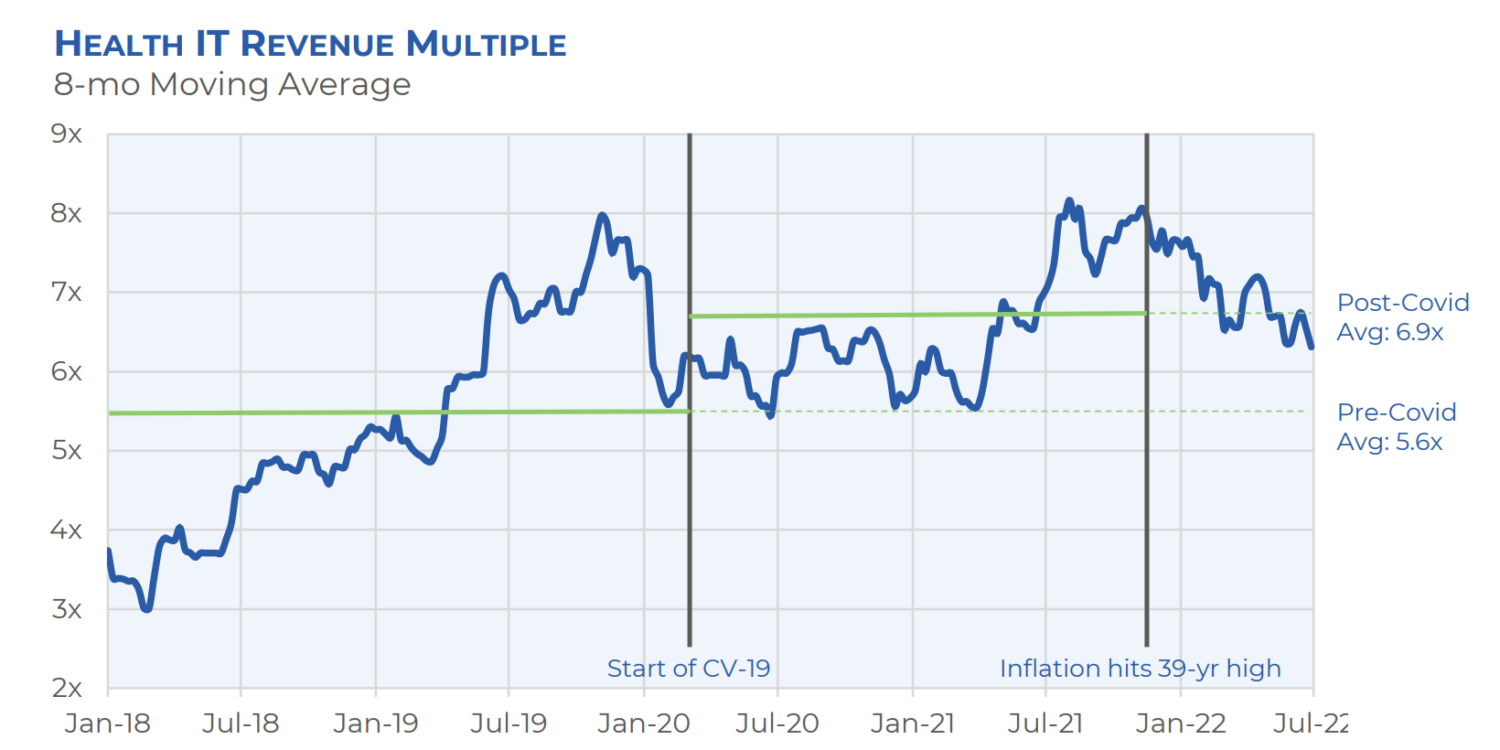

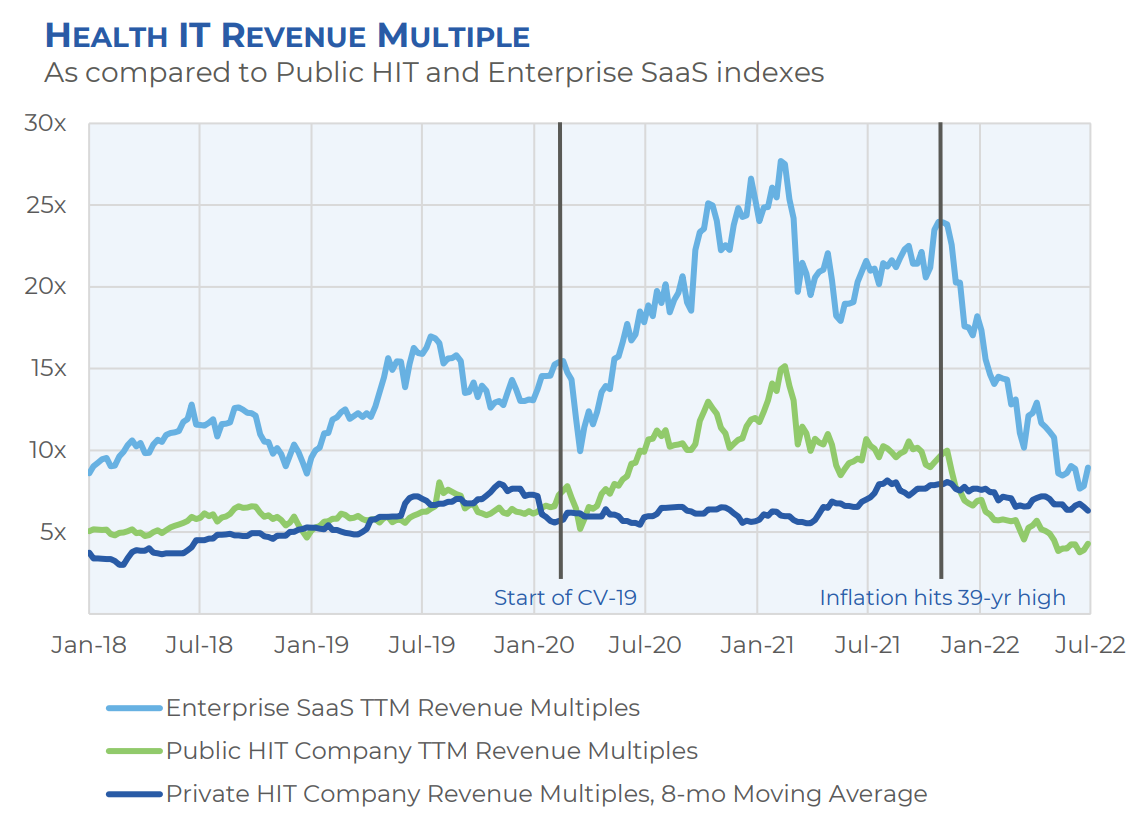

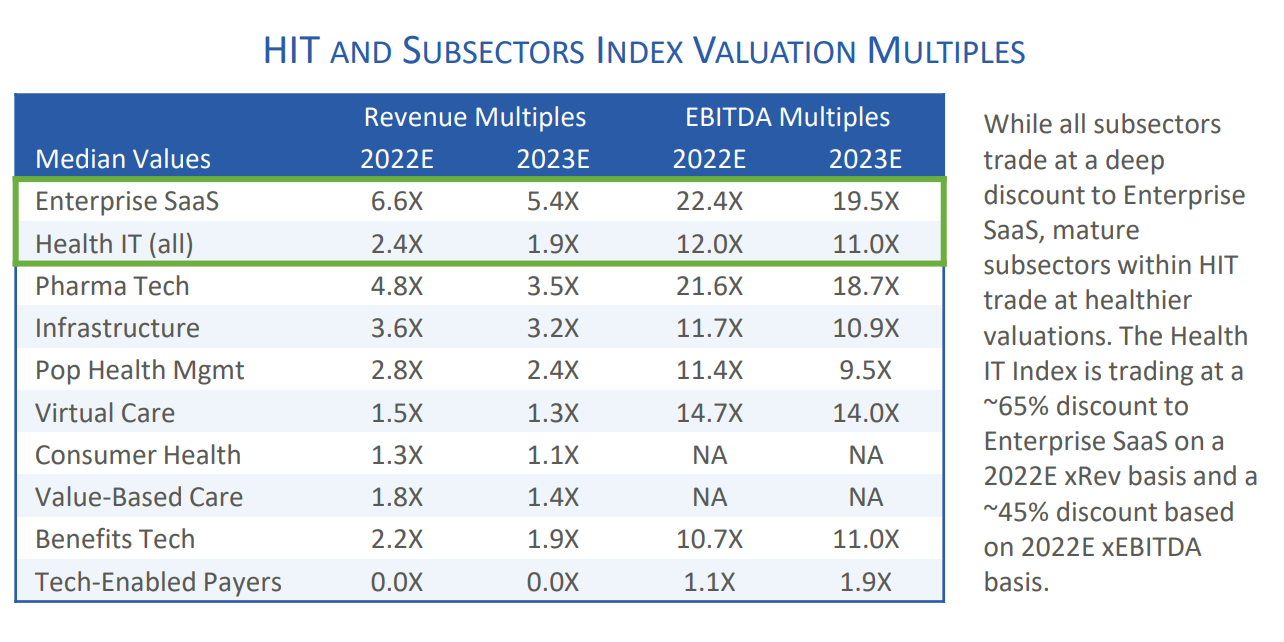

Valuations are undeniably falling but remain at a very high level when put into a historical context.

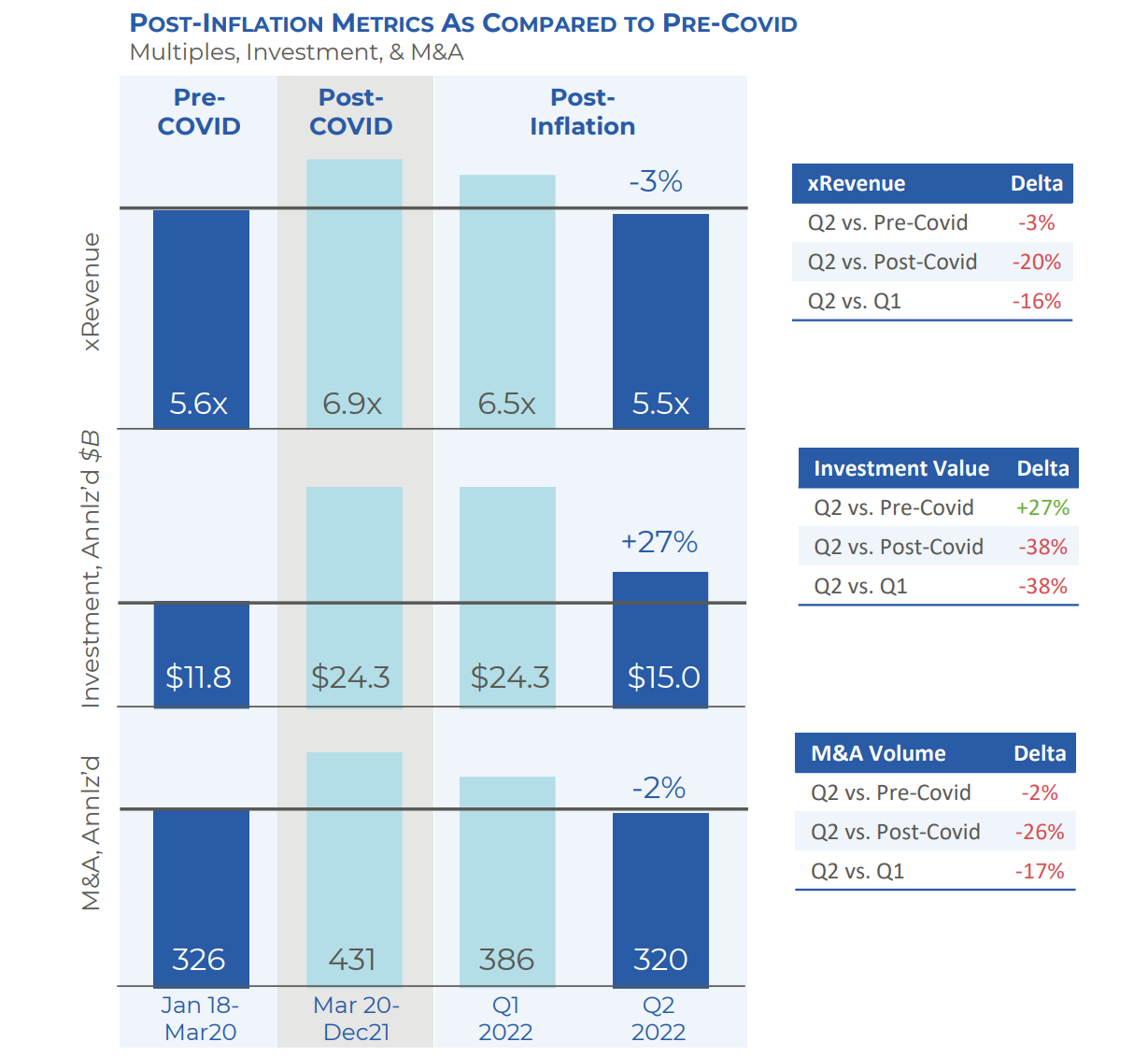

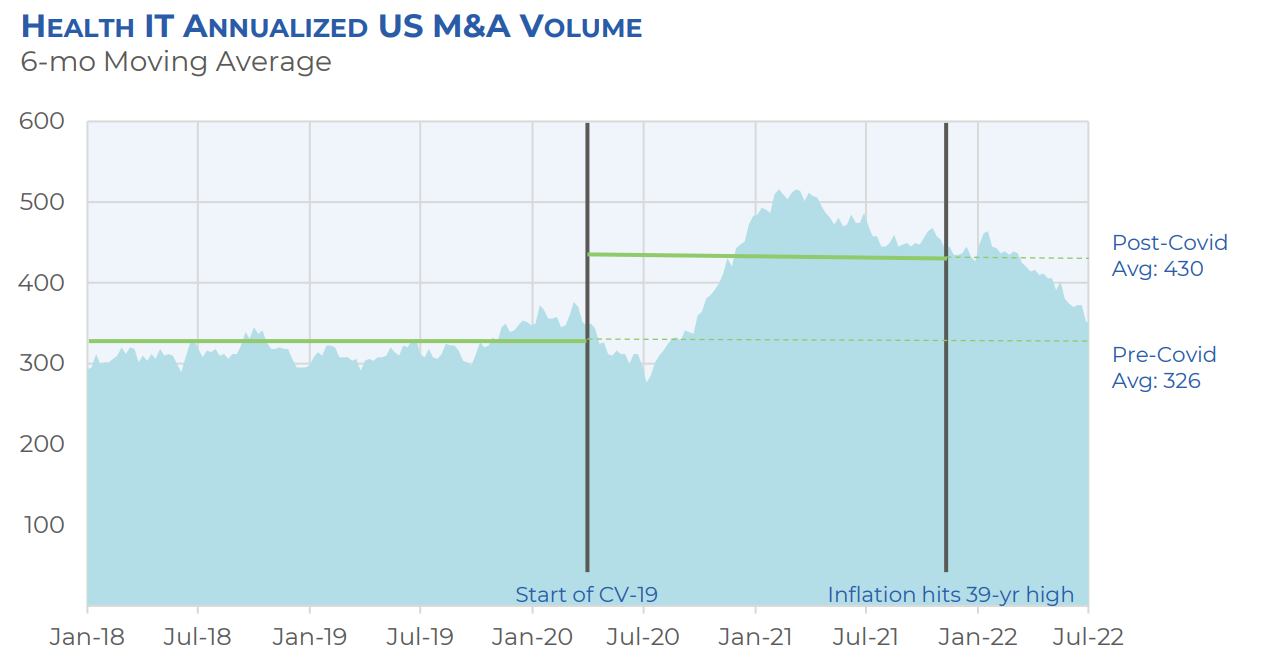

Despite gloomy headlines and the seemingly harrowing declines in valuation, it’s important to not lose sight of the steady climb in valuations since the beginning of 2018. Comparing Q2 vs. Q1, the 16% decline feels sharp, though begins to feel like a softer landing when compared to the average experienced in the pre-COVID period. Further, when looking at 8-month trailing data (see the chart on page 3), valuations today continue to be ~70% higher compared to the 8-month trailing multiple from January 2018. It is important to note that one-quarter of data is not indicative of a trend, though we appear to be on a downwards trajectory and may not have yet hit the bottom.

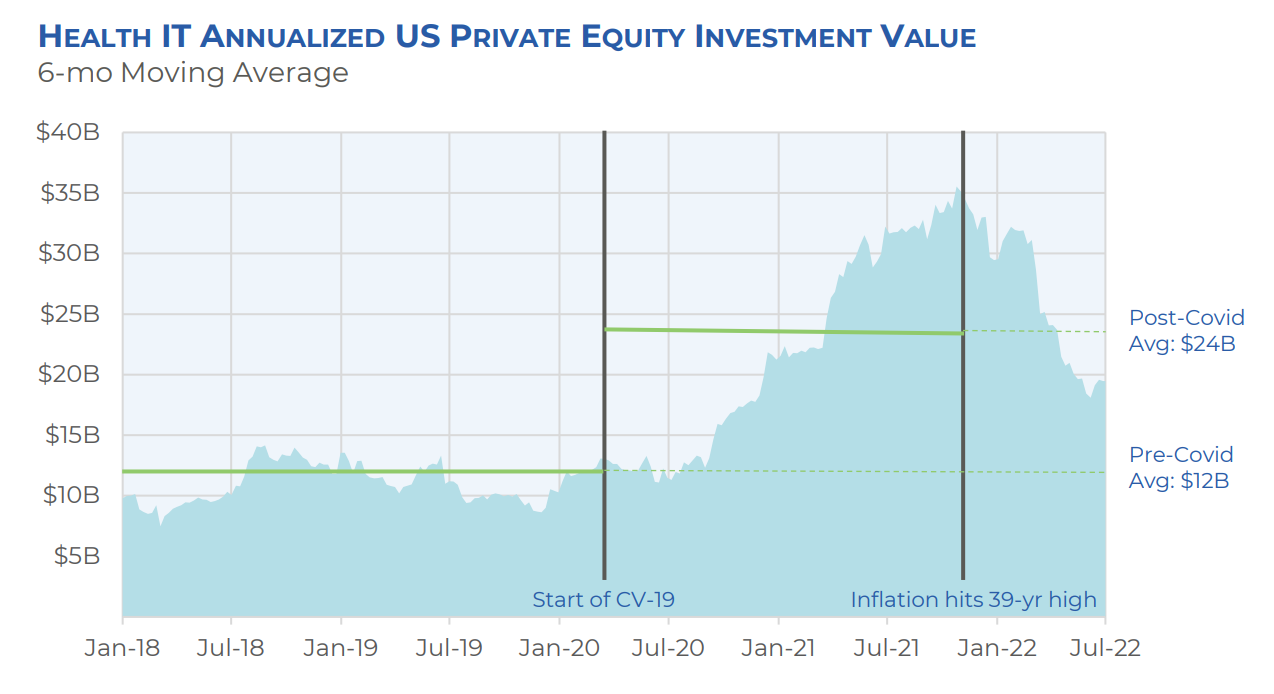

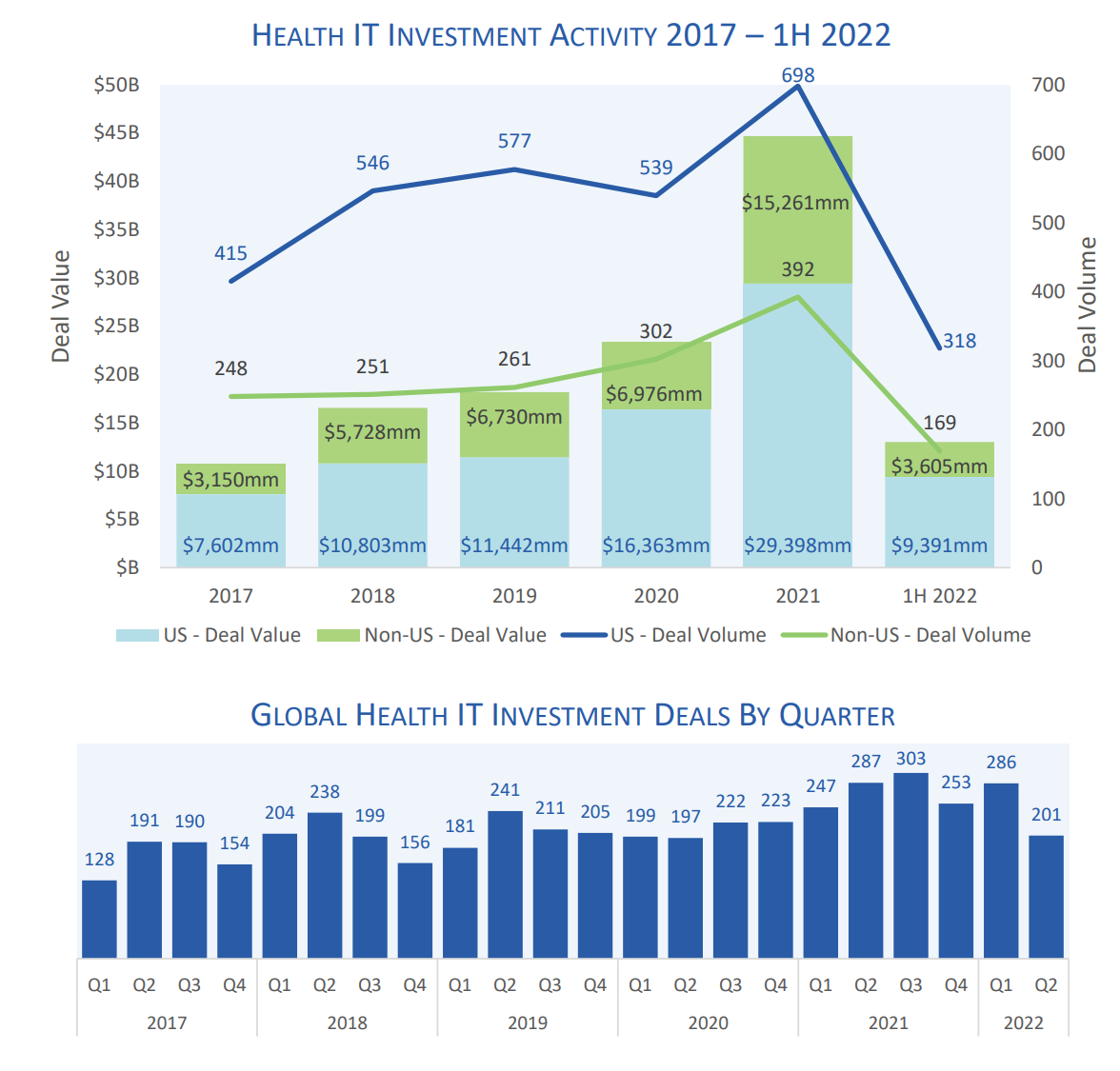

The amount of investment going into Health IT is nearly half the Post-COVID peak, but still 27%

higher than Pre-COVID levels. In 1H 2022, US-based health IT companies raised $9.4B, which is 40% below 1H 2021, but still 46% higher than the amount of investment seen in 1H 2019 (see the chart below for more detail on T6M data).

Private company valuations are much more stable than public company valuations. Private company valuations did not experience nearly the same level of Post-COVID euphoria nor are they declining as precipitously. In fact, comparatively, private company valuations appear almost flat against the high volatility of the public equity Health IT and SaaS valuations. However, the impact from declining public company valuations is now being felt in the private sector, representing the historically consistent two-quarter lag.

The cumulative overhang of private equity capital peaked in 2020 and has declined modestly since, but remains at historically very high levels, indicating that there is substantial capital on the sidelines. Dry powder peaked at $846 billion at the end of 2020, and declined to $819 billion by the end of 2021, and is now sitting at $749 billion.

The private debt market is tightening. The rising cost of debt makes financing more expensive, increases the share of equity required for transactions, and ultimately puts further pressure on valuations. The cost of debt has more than doubled for B-rated issuers (junk bonds) in 2022. The debt financing environment has become so tight that larger banks have effectively exited the market, leaving the debt financing to private lenders.

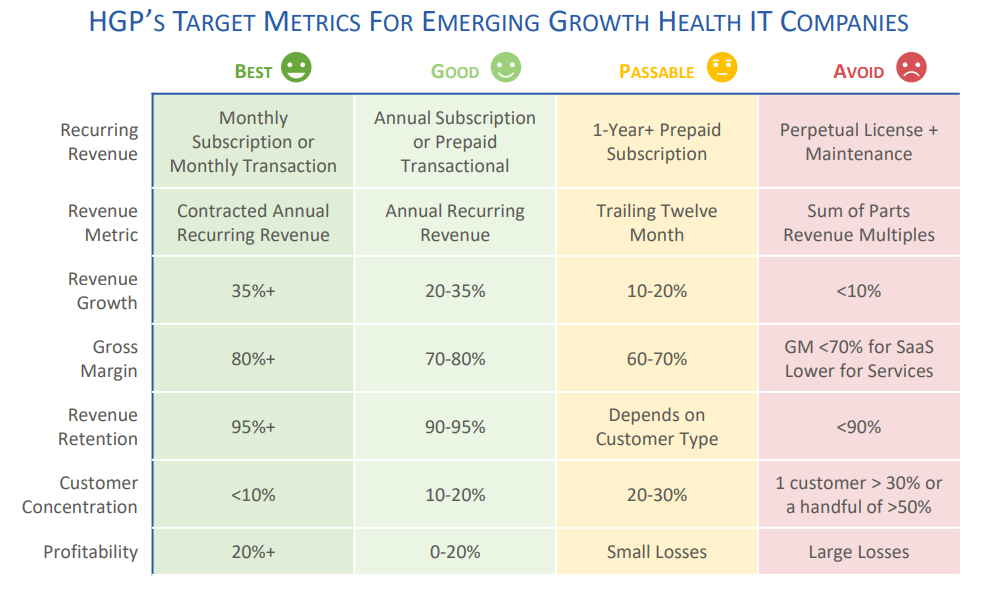

Quality is at a premium. Valuations remain historically strong for high-quality assets, seeing little impact Post-Inflation. See our table on page 12 with the typical criteria for the “best” health IT assets. While less frequent, HGP continues to see quality companies fetching superior valuations.

However, the criteria for a “quality company” has been raised to a higher standard. During PostCOVID euphoria, investor investment standards slacked, and many lower-quality companies received high-quality valuations. In Post-Inflation, investors have been less forgiving, causing companies that no longer meet the thresholds to experience lower valuations as compared to their superior-performing counterparts. As a result, more lower-quality companies are failing to transact in current market conditions either due to a lower valuation or declining levels of interest.

All else equal, profits are at a premium over growth. All things equal, EBITDA multiples are holding stronger than revenue multiples. Companies expecting to trade on revenue multiples are facing more scrutiny over their ability to scale, and the hypergrowth strategy is no longer being rewarded.

Fewer investors are stepping up, but there is a strong enough capital overhang to keep valuations high. In a competitive process involving multiple investors or acquirers, a smaller share of suitors is delivering high valuations, but the share is still sufficient to support higher valuations overall. If support from premium buyers declines further, valuations will feel more pressure.

The M&A and capital investment thesis remains strong. While investors and acquirers are more cautious, they generally remain in active pursuit of investments and acquisitions. Processes continue to start strong and receive a high degree of interested parties, but both acquirers and investors are tightening their investment standards.

The private debt market is tightening. In our conversations, lenders indicate that the cost of debt is rising, but demand remains high despite a decline in leveraged buyouts. Like equity investors, lenders are more cautious and hold higher standards for quality.

Industry consolidation will be fueled by low public company valuations and create opportunities for ongoing market share consolidation or big strategic moves. Smaller companies that were raising large amounts of capital and feeling bullish about going up against the large incumbents may struggle to access capital and become prime acquisition targets for the incumbents.

Companies that raised premium-priced capital Post-COVID may struggle as they face the need to shift away from a growth-at-all-costs business model and are forced to make workforce and cost reductions and potentially face dilutive down rounds. In some respects, this will result in a healthy reduction in disruptive yet unsustainable strategic practices.

Companies who did not pursue a growth-at-all-costs strategy and have instead successfully proven their ability to scale will benefit as competitive pressures ease, resulting in improved pricing pressure and customer acquisition cost dynamics as underscaled competitors shake prove to be unsustainable.

While valuations are falling, HGP believes multiples are nearing the bottom, but we do not expect a significant bounce back. We think a return to post-COVID euphoric levels is unrealistic, and investors and sellers need to detach themselves from those expectations. We expect valuations to settle back into the 2018-2019 range, near where they range today although with more forgiveness and support for breakeven growth companies than the market is providing today. It is worth noting that the Fed Funds Rate peaked at 2.42% in 2019 and valuations were not under pressure at the time, and we believe that further rate hikes are reaching a point where they are priced into current valuations.

During the Post-Inflation period, winning sectors are those that benefit from a down market, such as supply chain management, spend analytics, contract and vendor management, lead generation, revenue enhancement (strong RCM tools, denials tools, payment integrity).

The market will shake out those who benefited from luck and timing from those with real ability following a decade of hyper-accommodating Fed policy.

A challenging and uncertain market environment will produce long-term benefits, teaching skills such as tenacity, discipline, adaptability, and patience that ultimately lead to more stable strategies and wise leadership in the future. Those that show the ability to adapt and respond to change will survive and emerge stronger.

Synthesizing Our Sentiment

The crosscurrents from macroeconomic and inflation data are challenging for even the most studied

economist to interpret, as fragmented and contradictory data points flood the news. Similar crosscurrents of data exist in the Health IT market. A strong appetite for investment and M&A persists, yet the appetite for risk is dramatically lower than a year ago. Any expectation for a return to Post-COVID euphoria is unrealistic, and as such, if the market settles at Pre-COVID levels, which is where it stands as of Q2 2022, we will consider this an excellent outcome. In some respects, the regression to historical norms is a healthy process for the market to return to patterns that are more predictable and sustainable. For now, given the falling trajectory as of Q2, we will monitor the data closely in search of the floor and the idealistic “soft landing”.

HEALTH IT MARKET TRENDS

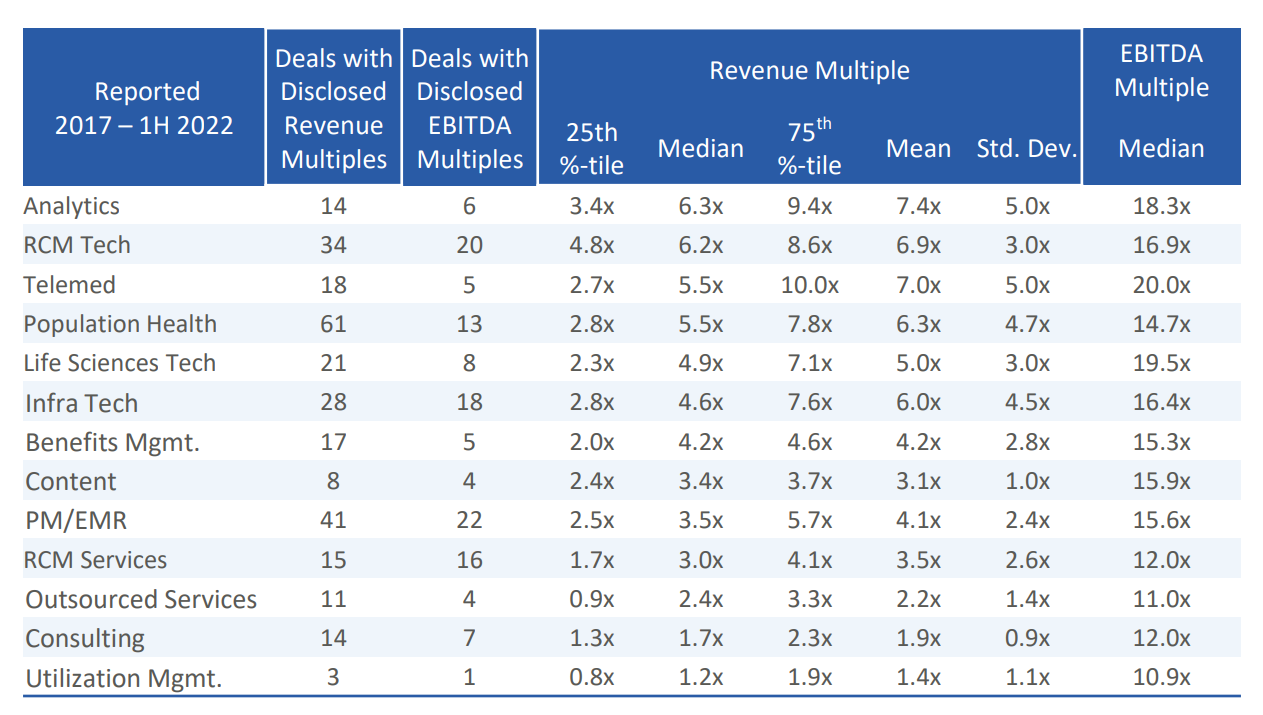

HGP keeps close tabs on M&A valuations to see how the market evolves over time. While we can only draw data from deals with disclosed multiples and therefore must be careful to consider bias in any conclusions we draw from this data, we can still get a good sense of how the market values companies within the different subsectors of health IT. The following table and accompanying box and whisker plot show the distributions of revenue multiples in 13 subsectors of health IT. The sectors were sorted according to median revenue multiple from largest to smallest.

We believe it’s important to keep dispersion in mind when assessing valuation data, which is why we include the 25th percentile, 75th percentile, and standard deviation in our summary statistics. While measures of central tendency like the median and mean are certainly indicative of how buyers are valuing assets, the dispersion shows that with higher multiples, we also see higher risk. This becomes especially apparent when we chart the data using a box-and-whisker plot. Generally speaking, the sectors with the highest median revenue multiple also experience large standard deviations and positive skew. For instance, while 25% of the observed telemedicine companies received 10.0x revenue or more in sale transactions during the period, another 25% received less than 2.7x revenue at exit. Companies in these hot spaces cannot forget that they still need to show strong operating metrics in order to realize premium valuation multiples.

In the first half of 2022, we have observed that a few sectors saw their median multiples tick up relative to the period between January 2017 – December 2021, namely Analytics (by 1.3x), Infrastructure Technology (by 0.9x), and RCM Services (by 0.7x). We see this as a possible indication of the resilient nature of the sectors, when juxtaposed with sectors that had benefited from COVID tailwinds, such as Telemed, where M&A activity has decreased by ~60% compared to 1H 2021.

The box-and-whisker plot graphically displays the Median, 25th Percentile, 75th Percentile, Minimum, and Maximum; where points beyond 1.75 times the Inter-Quartile Range are shown as outliers. The inter-quartile range is represented by the “box” and shows the range between the 75th Percentile and the 25th Percentile. Visually, the inter-quartile range serves to describe the variability of the data. Note that point estimates such as the mean or median can often be misleading on their own, as they do not convey the level of variability which can be very high such as in the Telemedicine and Population Health sectors.

The sectors were sorted according to decreasing median revenue multiple and show a trend of decreasing IQR as median revenue multiple decreases. Thus, while companies that fall within sectors further to the right on the graph can expect a lower revenue multiple in a transaction, the transaction outcome is also more predictable. A company that falls within a sector on the left, however, cannot have as strong confidence in their expected outcome. These observations follow a common theme in investment theory: that with greater potential upside, there is also greater risk and volatility.

While the metrics presented here may be used as a guidepost for expected outcomes, the end result of any transaction often depends on buyer circumstances as much as on seller or market fundamentals, and buyer circumstances tend to be extremely unpredictable. It is not uncommon for the clearing price of a transaction to be significantly higher than the cover bids. This usually occurs when a buyer has unique circumstances that justify a higher price than the rest of the buyer universe. Identifying those buyers and appropriately positioning in relation to them is part of the art of running a successful transaction process.

The following table provides additional context on the valuation trends within each sector as well as a

sample of recent transactions within each.

HGP has observed a number of tangible and intangible company and transaction characteristics that typically define where a deal falls on the valuation distribution. Growth, profitability, and recurring revenue are the most commonly identified factors used to justify valuation multiples. Not all health IT companies capture premium valuations just because they operate in health IT. However, those companies that offer a combination of growth, address an unmet need, and fit into the vision of healthcare reform are seeing valuations significantly higher than historical patterns of activity. Premium value is also created when a seller fulfills the specific needs of a buyer at a specific point in

time. Timing and serendipity are external factors that play a large and sometimes unpredictable role

in the creation of value.

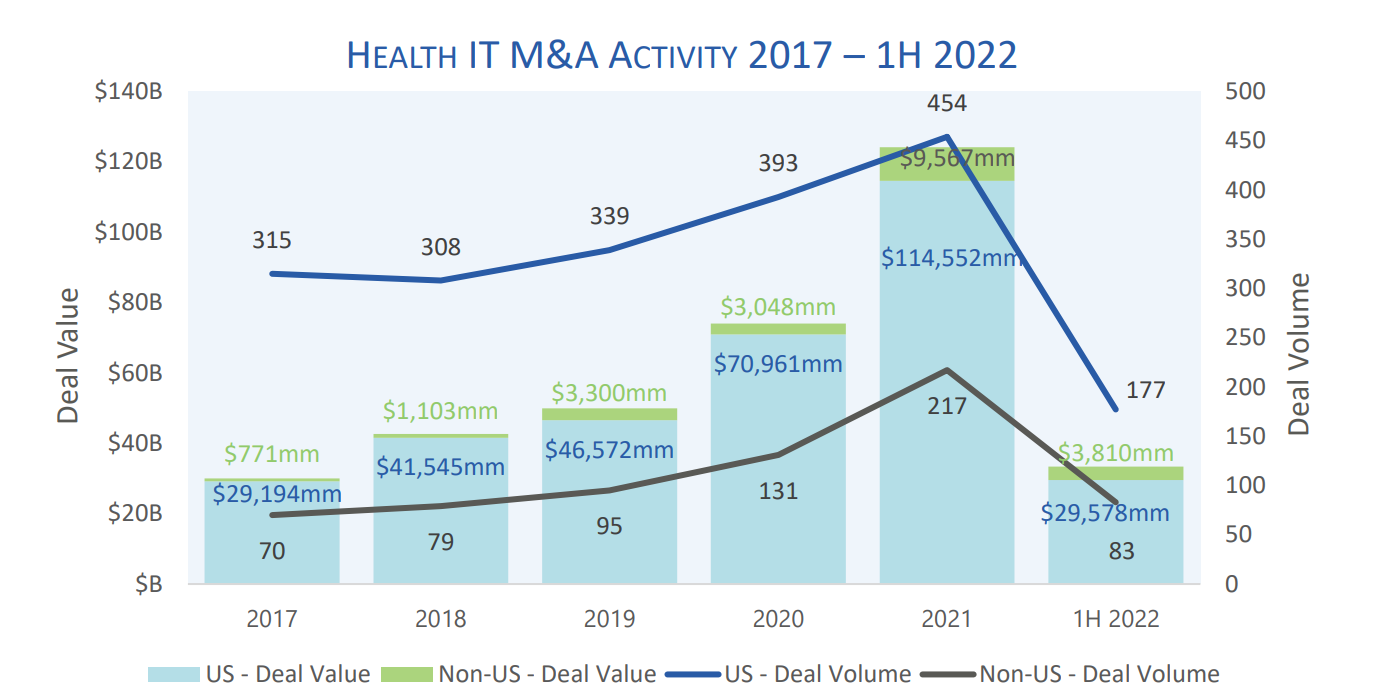

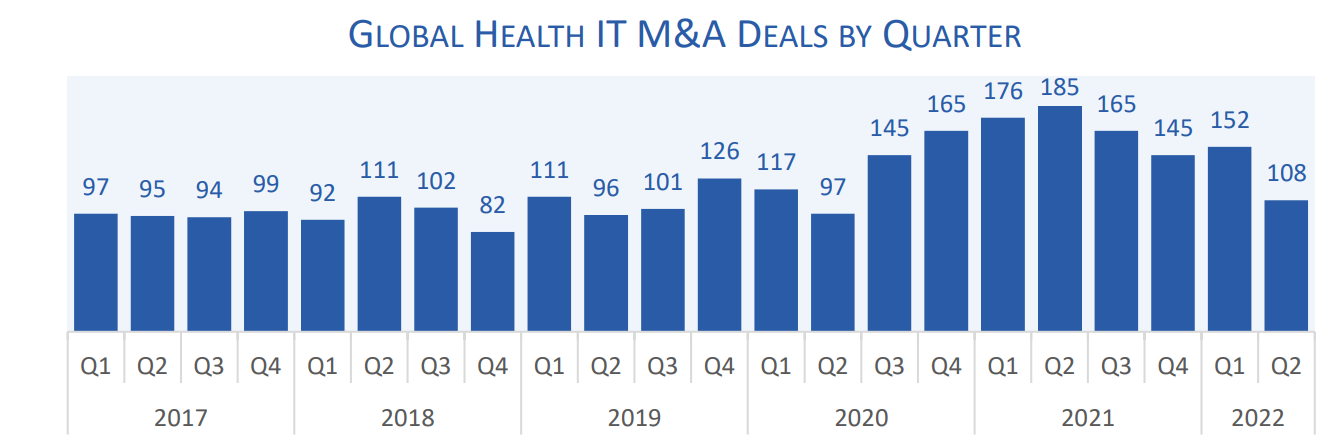

The M&A frenzy of 2021 seems to be over at the onset of the market correction era: compared to 1H 2021, deal volume and value declined by 28% and 30% in 1H 2022, and quarterly deal volume in the US dipped below 100 for the first time since Q2 2020. However, it is imperative that we put these statistics in perspective. Compared to the period between Jan 2018 – March 2020, deal volume and value in the US are up by 8% and 45% respectively. Therefore, while the pullback shows nervousness and pause on the buyers’ side, the level of activity still hasn’t fallen back the pre-COVID norms, and deals that are happening are happening at high valuations.

It is worth noting that 2021 deal value skyrocketed due to few mega-deals: Cerner, Nuance, and athenahealth marked three out of five largest Health IT M&A deals in history and constituted almost half of the entire deal value for the year. Notable transactions in 2022 included Ensemble Health Partners (Berkshire Partners), Cloudmed (R1 RCM), and Vocera Communications (Stryker). It’s important to note that M&A deal value is a metric largely impacted by mega-deals, and thus deal volume is a preferable indicator when assessing market momentum.

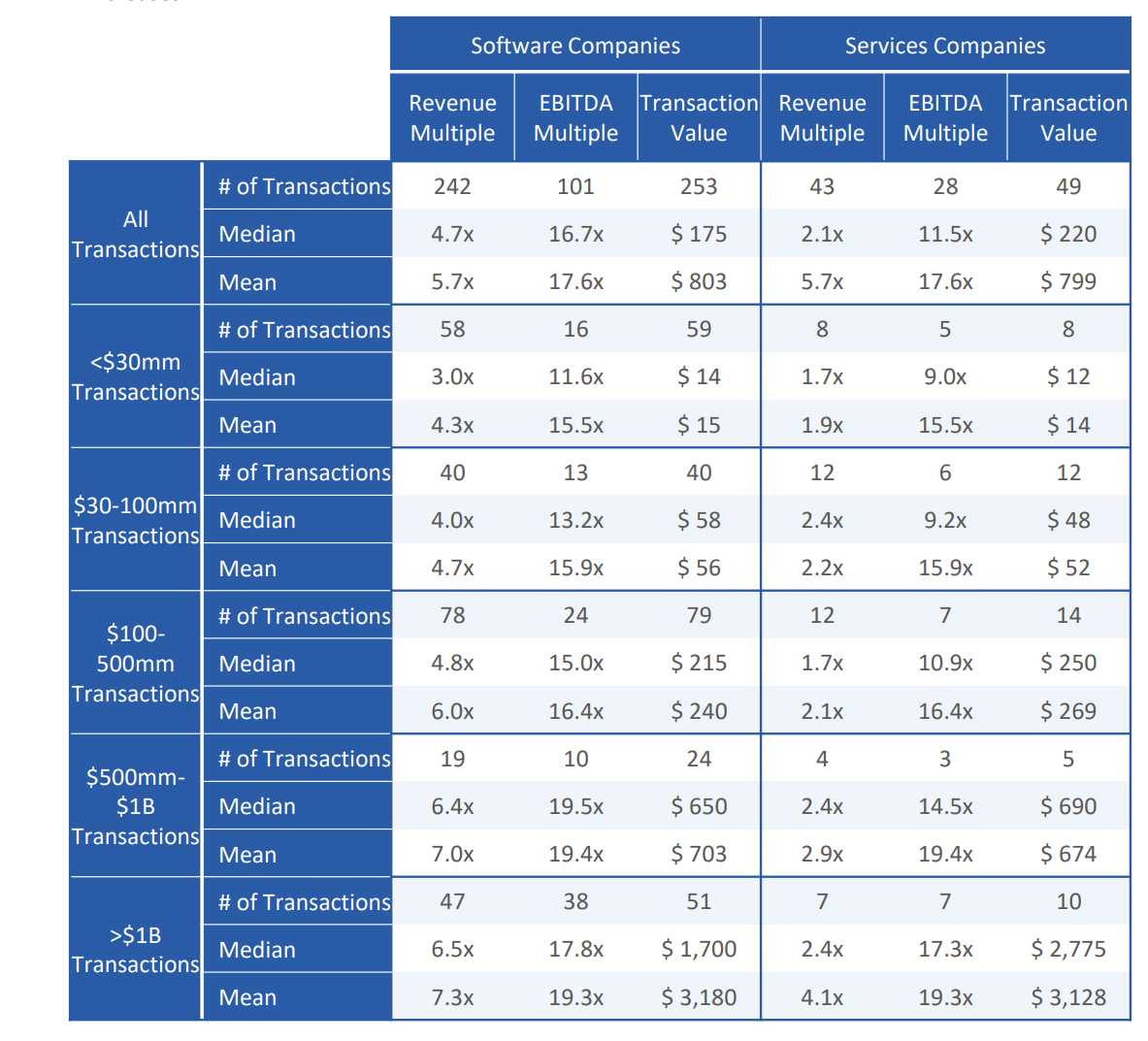

Getting more granular into valuation multiples, it is useful to note that multiples are often somewhat correlated to a target’s enterprise value. Software company valuations steadily climb as enterprise value increases until approximately the $1B valuation mark. Services company multiples experience a similarly steady climb in EBITDA multiples, and in larger increments at the $500mm and $1B valuation marks. The inflection points are in part due to a private equity universe that has expanded leverage capacity for larger transactions, which in turn drives up valuation multiples as the enterprise value increases.

Generally, companies have three valuation inflection points: proof-of-concept, growth scalability, and

mature scalability.

1. The proof-of-concept is value created when a company shows that its product can be successfully

sold and deployed in a commercial setting.

2. Growth scalability occurs when an earlier stage company begins to show profitability or at least

scale at high levels of growth, although the organization is still small and lean.

3. Mature scalability takes place after a company has matured to a level where it takes on real

corporate and organizational infrastructure and the company begins to show strong profitability.

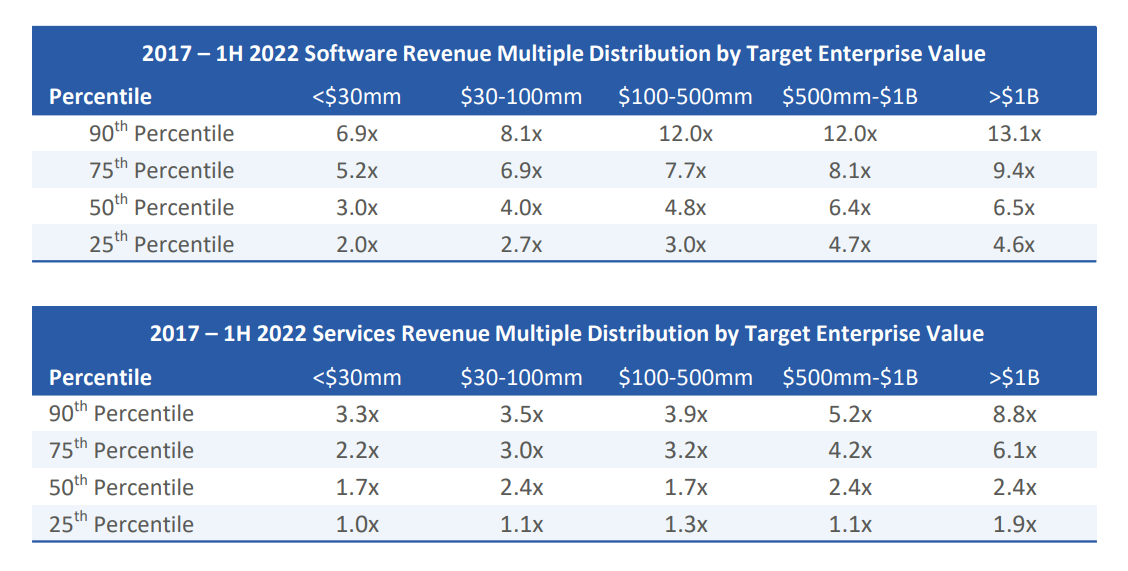

The above tables demonstrate the positive relationship between valuation and scale. As software businesses grow in scale, so do their multiples. Revenue multiples steadily increase from 3.0x to 4.8x as companies begin to reach the $100mm mark. As software businesses grow further to over $500mm and reach mature scalability, they experience a material step up in value, with revenue multiples further increasing to a median of around 6.4x.

Services businesses do not seem to benefit as drastically from increased scale as do software companies. While median revenue multiples do not rise substantially as services companies mature, premium assets (such as RCM Services) seem to be rewarded for scale as they fetch steadily rising multiples in the 75th and 90th percentiles, going as high as 8.8x for companies over $1 billion in enterprise value.

Detailed multiples trends can be found in the following bar charts. It should be noted that valuation multiple trends can be very volatile given the limited availability of data.

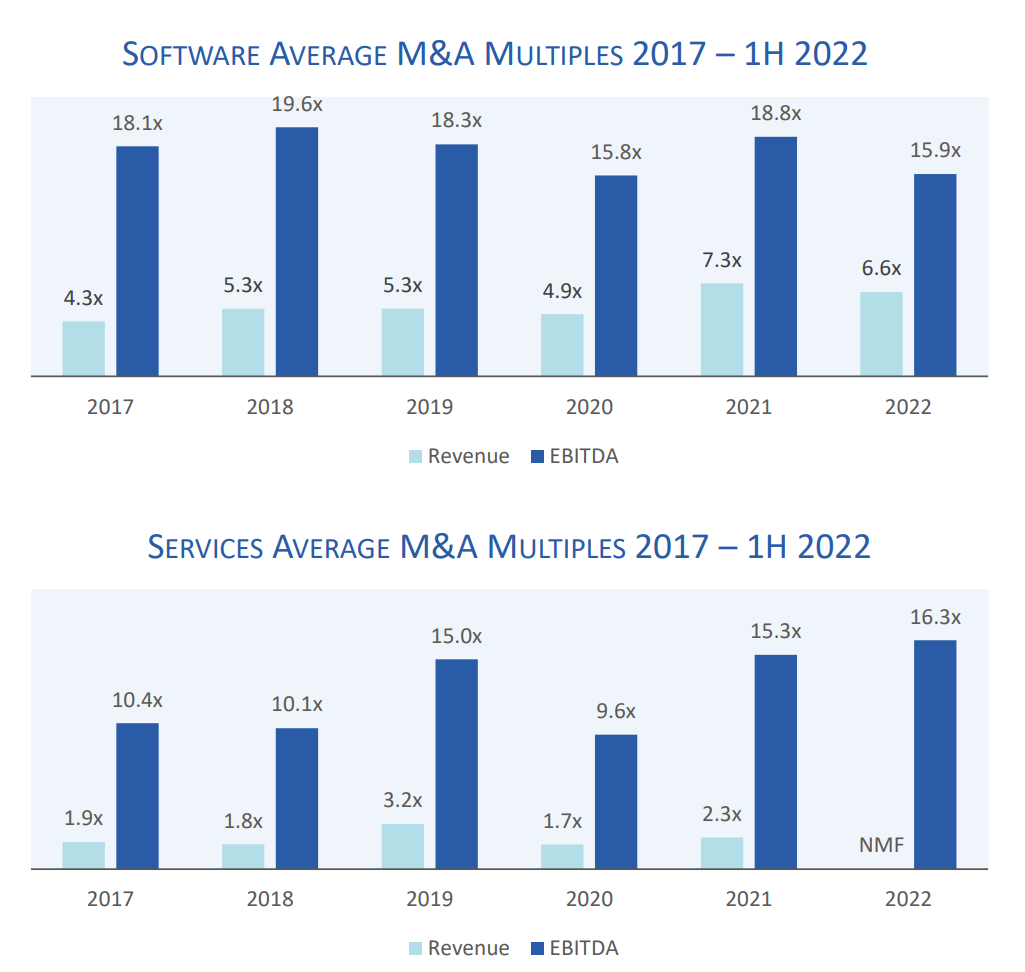

While we would traditionally expect valuations to be higher for software companies, 2022 presents an anomaly with a higher reported EBITDA multiple for services. Delving into the dataset, there is a small sample size of 6 services transactions mostly comprising high-quality mega deals. These include Aspirion, CloudMed, Ensemble Health Partners, and Revecore. Due to the large size and high quality of these transactions coupled with the limited number of transactions in the dataset, the 2022 EBITDA multiple for services may not be a reasonable valuation indicator for services transactions on the whole.

HEALTH IT CAPITAL RAISES (NON-BUYOUT)

Capital raise activity echoed the M&A market: not as frothy as 2021, but still above the pre-pandemic average. HGP monitored 487 capital raise transactions in 1H 2022, representing $13.0 billion in value globally, marking a 50% decrease from 2021 levels; however, when compared to the first halves of 2018, 2019, and 2020, this year outpaced them 48%, 38%, and 60%, respectively. We expect investment activity to stay higher than pre-pandemic levels since record venture fundraising in 2021 equates to capital being deployed for years to come; however, factors like the closed IPO window and declining valuations will distribute those funds across more start-upsto diversify risk.

HEALTHCARE CAPITAL MARKETS

HGP tracks a custom index within the health IT space. What classifies a company in the universe of

health IT, and ideally creates a valuation premium, is a strong information technology and data

component that creates scalability and competitive strength. This is particularly relevant to services

organizations that use technology and data analytics to streamline their operations. With this in

mind, HGP evaluated the performance of publicly traded health IT companies against the S&P 500

and the Nasdaq indices, in order to assess the health IT companies within the wider market.

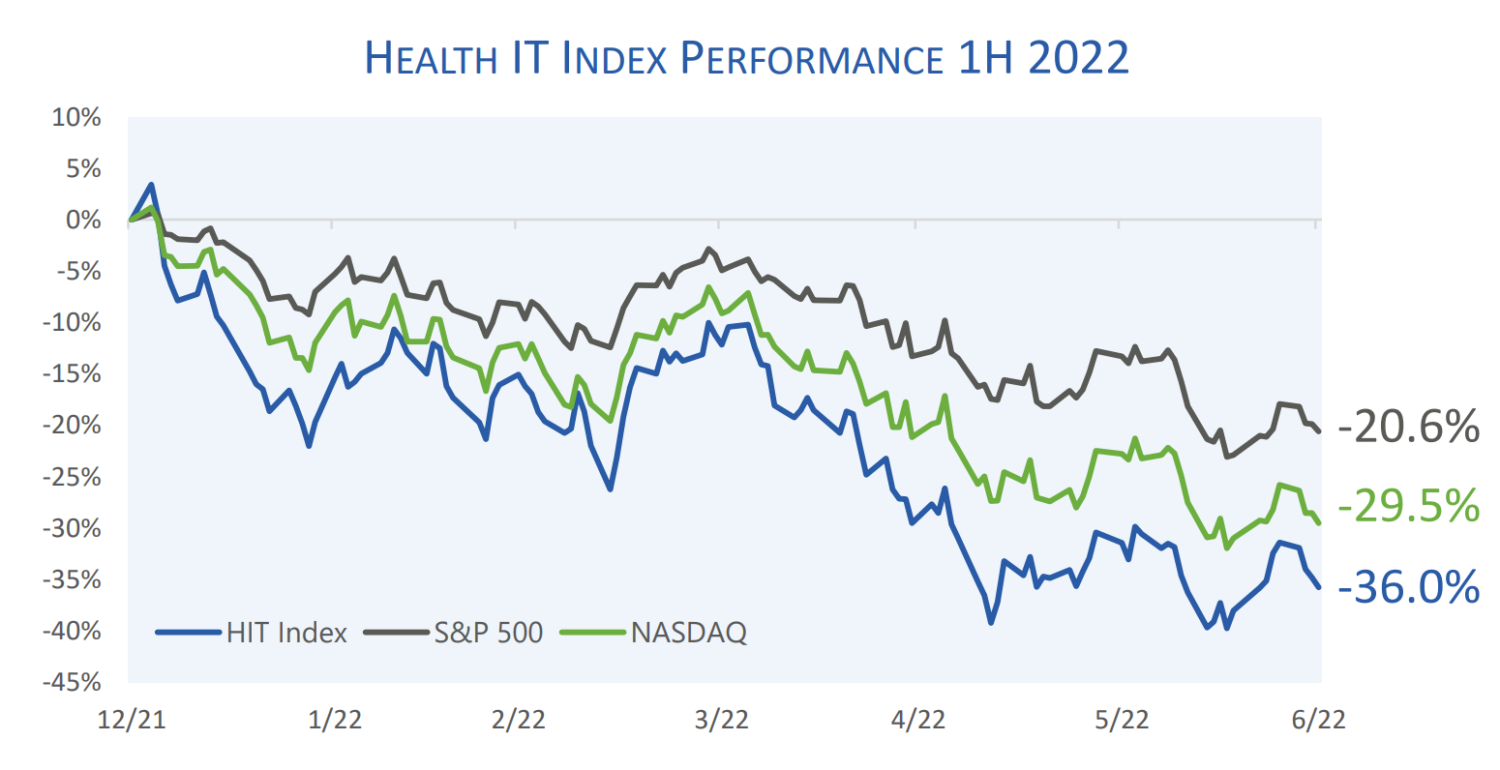

Public HIT companies were not spared in the market downturn that began in January 2022, losing an

astonishing 34% over the last 6 months, with an overwhelming 56 out of 68 tracked companies

ending the first half of the year with negative returns. Although public health IT companies

undoubtedly endured the systematic market pressures felt across the broader markets, it is

important to acknowledge the unique dynamics impacting the health IT space.

As we saw in 2021, the post-pandemic era saw a massive amount of capital pumped into private

markets, fostering a highly competitive environment, crowded by private-equity backed companies

operating under a growth-at-all-costs mindset. In 1Q 2022, we began to see cracks in this new

environment: customer acquisition costs began to rise as more companies in the arena were fighting

for members, access to clinicians continued to be exacerbated by supply constraints, pricing pressure

was acutely felt due to the intense competition, and sales cycles were prolonged in many endmarkets. Private companies seemed to get away with playing by a different set of rules for a number

of months, creating a disadvantage for the public comps. While we have started to see private

investors refocusing their criteria to catch up to the public markets, the lag was acutely felt by public

markets and created unique headwinds, amplifying the downturn seen in 2022.

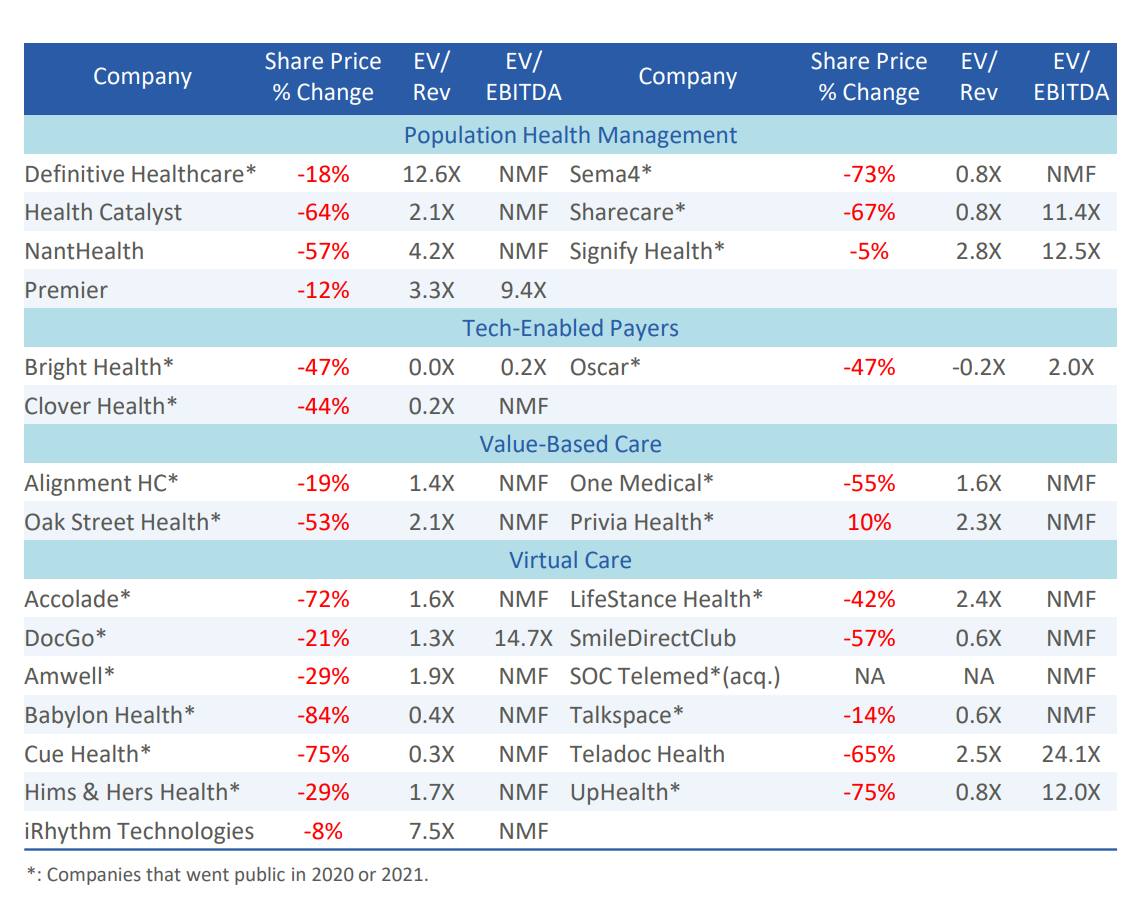

It’s worth noting that the HIT Index is composed of 34 companies that entered the market in 2020 or

later. These new entrants have been especially volatile, with IPOs and SPACs declining 40% and 48%,

respectively.

HIT & SUBSECTORS INDEX PERFORMANCE 1H 2022

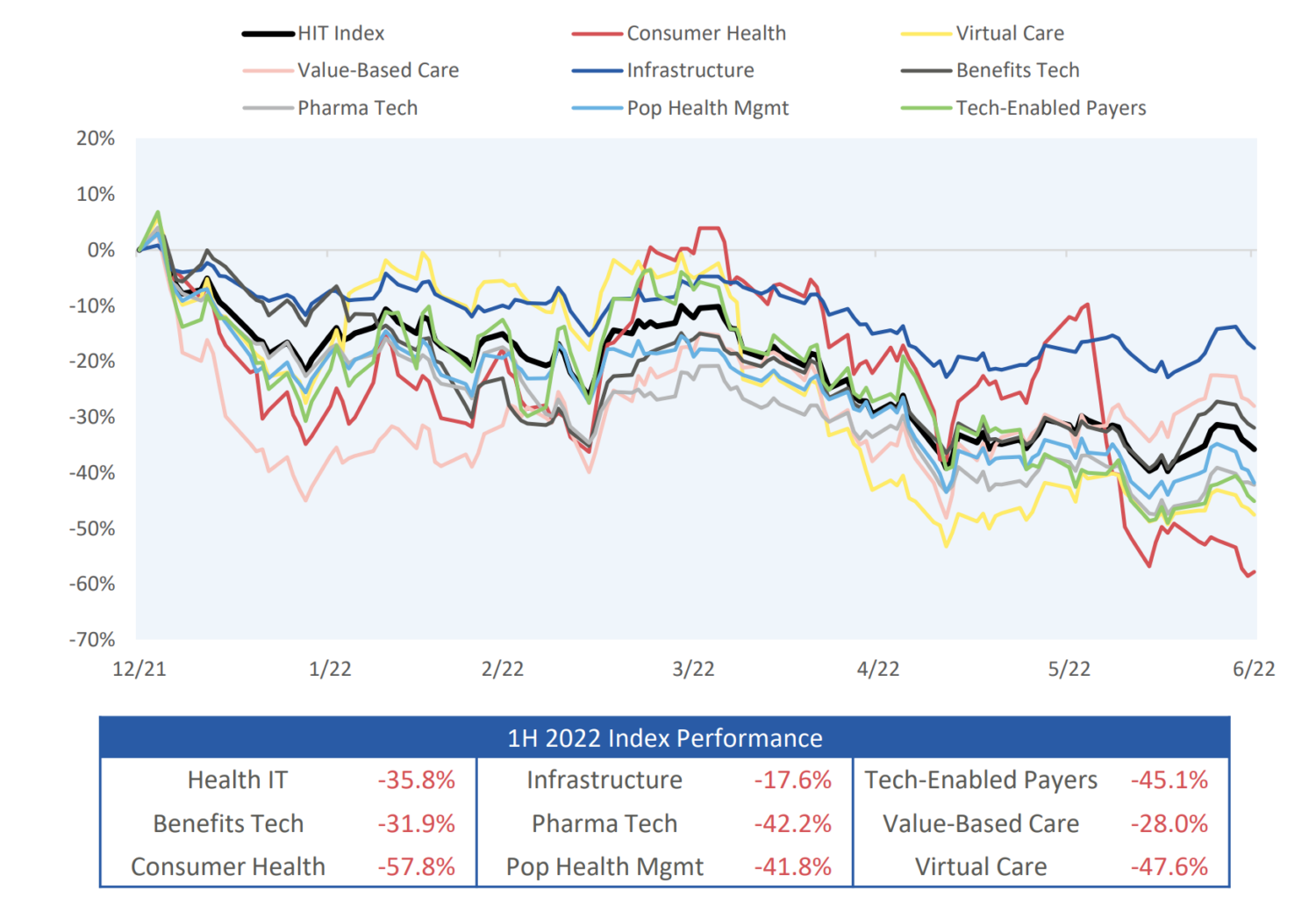

To drill-down into the drivers behind the variability within the Health IT index, HGP classified the 68

constituents into their respective sectors – Benefits Tech, Consumer Health, Infrastructure, Pharma

Tech, Population Health Management, Tech-Enabled Payers, Value-Based Care, and Virtual Care.

Though every index has lost value in the double digits, the Infrastructure basket stands out from the

mix as the only sector to have outperformed against the major market indices, largely benefitting

from its seasoned and value-based make-up. The sector differs from the others in two distinct ways:

1) only 11% of the constituents represent companies that went public since 2020 (as compared to

45% – 100% in the others); and 2) the sector did not benefit from COVID-19 tailwinds in the peak of

the pandemic as much as the other sectors, and thus, did not see a drastic correction once those

tailwinds subsided. The relative success of these companies that tend to be bigger, profitable, and

core technologies is an indication that the market has pivoted towards rewarding profit over growthat-all-costs.

Other sectors have underperformed the market by a thick margin, as their high-multiple growth

constituents took major hits due to their high sensitivity to interest rates and inflation. Despite the

rocky performance across the board, HGP expects investor interest in Health IT to remain strong, as

we continue to see an indisputable market thesis for Health IT.

HIT AND SUBSECTOR INDEX PERFORMANCE DETAIL AS OF JUNE 30, 2022

Detail on the sectors and companies HGP tracks as part of the health IT index can be found below. Multiples shown are based off 2022E revenue and EBITDA.

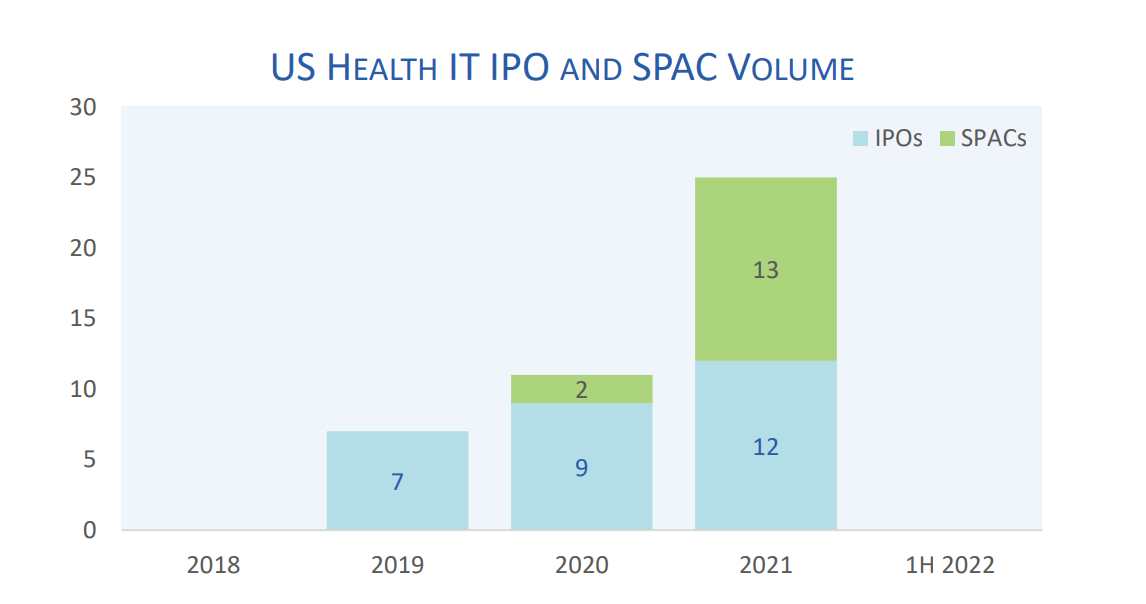

HEALTH IT IPOS AND SPACS

“We believe this is a Crucible Moment, one that will present challenges and opportunities for many.

First and foremost, we must recognize the changing environment and shift our mindset to respond

with intention rather than regret.” Sequoia Capital, Adapting to Endure Presentation, May 2022

In no segment is the market dynamic more dire than the IPO market. The US IPO market is coming

off its slowest quarter since 2009 with continued deceleration throughout the second quarter.

According to Bloomberg, companies raised $4.9 billion in 1H 2022, less than 6% of the record sum

raised in the first half of 2021. Although 2021 was an outlier year, 1H 2022 still pales in comparison

to the 5-year 1H average of $47 billion. Over 90% of companies who went public via IPO in 2021 are

trading below their offer prices, with the average trading down 44%.

SPACs faced a similar story – after 589 SPAC IPOs in 2021, 1H 2022 saw only 27 SPACs. From a Health

IT perspective, there were no public listings in 1H 2022, marking the first period without a public

listing since the drought year of 2018.

With stock markets suffering the worst first half since 1970, the doors are virtually closed to public

market exits. This reality is particularly difficult for late-stage companies that raised capital at frothy

valuations in 2020 and 2021 with aspirations to go public. On the other side of the table, IPO

conditions have proven to be particularly challenging for crossover investors. Crossover investors

typically seek higher, shorter-term investments in the round immediately prior to an IPO. The

investment category exploded during COVID, led by marquee names such as Tiger Global and Insight

Partners as well as many large mutual funds, such as Fidelity and T. Rowe Price. These funds also

provided liquidity to early-stage investors, making these rounds of financing an increasingly pivotal

part of the capital cycle. As the IPO drought continues to play itself out, the future remains very

precarious for both late-stage companies and the investors who bankroll them. A sign of hope is the

growing backlog of 185 IPO registrations. Should the market provide an opening, there is plenty of

demand for new public listings. However, not a single Health IT company is in the hopper.

MACROECONOMICS

If 2020 and 2021 can be characterized as a market extravaganza, 2022 is felt as a hangover. Though we

had begun to see signs of the market cracking towards the end of 2021 across growthy sectors, 2022 has

been marked by a tough turmoil that has not been experienced since the Great Recession. As the

pandemic’s hold grows weaker around the globe, new economic disruptors have entered the stage,

namely inflation and geopolitical instability, in addition to the ever-present supply chain issues.

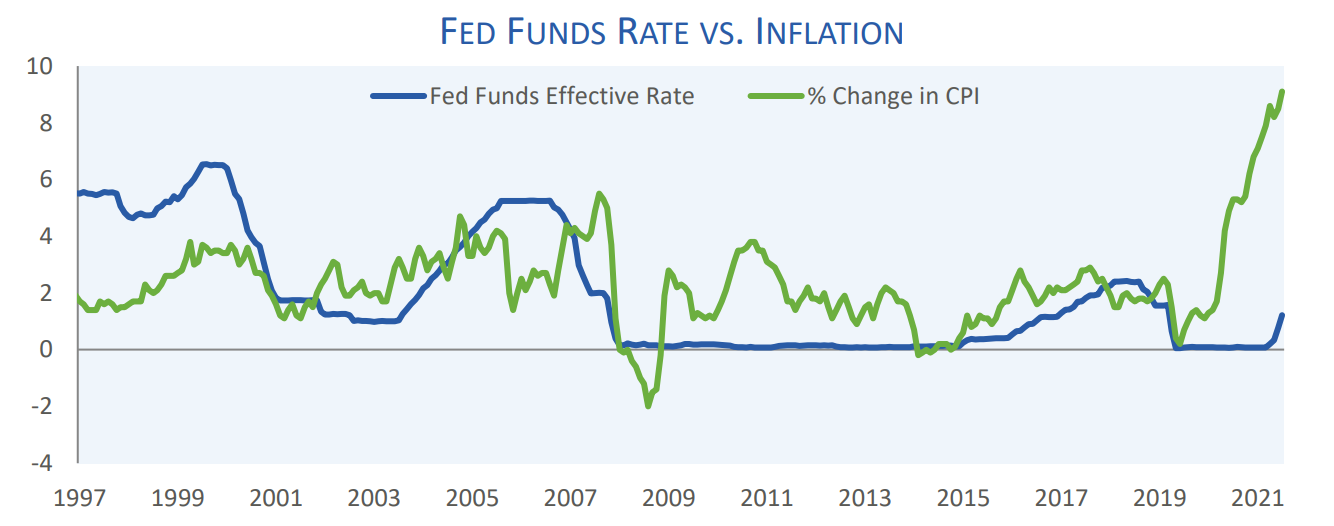

Inflation, which lay at or below the targeted 2% level for the better part of the last decade, started

breaking its shell in Q2 2021, which was largely welcome as a positive indicator of economic growth and

recovery from the impact of the pandemic. However, when the rate reached 6.8% in November 2021,

the severe challenge the Fed was now facing became apparent. The escalation in 2022 did not slow

down, with June seeing a record peak of 9.1%.

Why is the US and the world experiencing so much inflation? Supply and demand imbalances from the

COVID-19 pandemic, an explosive Fed balance sheet, and high energy prices taken together resulted in

significant and rapid price escalation. In more granularity…

Supply-Side Issues

▪ Ongoing COVID lockdowns in China and globally exacerbated supply chain issues stemming

from the original COVID lockdowns.

▪ Unemployment is at a 5-year low driving very tight labor markets.

▪ Russia’s invasion of Ukraine caused a spike in energy prices, which historically are a root cause

for most inflationary environments. Energy prices must be contained if inflation will be

contained.

Demand-Side Issues

▪ Household spending and business fixed investment remains strong.

▪ With low unemployment, wages are gaining but at a lower rate than prices overall.

▪ Post-COVID, the Fed ballooned its balance sheet, caused direct transfer payments from the

government to households, and cut interest rates to near zero.

Combatting such high rates of inflation had not been the Fed’s primary objective for the last 20 years,

but it has been signaling decisive action against inflation since the first benchmark interest rate hike of

25 basis points in March and a second one of 75 basis points in June, marking the most aggressive rate

increase since 1994. In the June FOMC meeting, the Fed officials indicated that they would raise the

target range on rates by another 175 basis points through 2022 and downgraded their GDP growth

estimates.

It is worth noting that compared to the inflation level, the Fed benchmark interest rate still seems low,

and could stand to aggressively rise to 2-3% levels to establish a higher neutral rate, instead of running

the risk of remaining “behind the curve” and not being able to reign in further inflation driven by wage-price spiral, launching inflation expectations into the “unanchored” territory.

Despite the rapid escalation in 1H 2022, most forecasts predict inflation will decline to a range of 5.5-

6.5% by year-end with further declines into 2023. The Federal Reserve aims to combat inflation while

not tipping the economy into a hard recession. Inflation averaged 2.4% for the last 20 years, allowing

the Fed the luxury to focus its policy on employment. The current environment, with inflation feeling

pressure from both supply and demand imbalances, is largely uncharted territory.

Under these circumstances of uncomfortably high inflation levels and correspondingly rising interest

rates, the equity market and the expectations that shape it have drastically worsened over the last six

months, following a sharp pivot into bear territory. The major indices of S&P 500, NASDAQ and DJIA

have all ended the six-month period with double-digit losses, at 21%, 30%, and 15%, respectively.

Technology stocks were particularly vulnerable to tightening expectations: more than 60% of all

software, internet, and fintech companies are trading below pre-pandemic prices, and a third are

trading below COVID lows, effectively canceling out gains.

When the public markets look grim, the sentiment trickles down starting with initial public offerings,

where the window seems to have closed until we start seeing positive indicators. Public equity raised in

initial public offerings in the first half of 2022 was a minuscule fraction of the activity in the same period

in 2021: 6%. Only $4.9 billion was raised in US initial public offerings, hitting its lowest since 2009.

Notable companies that went public this year were TPG, the private equity firm that is now minted an

alternative asset manager, and Bausch + Lomb, the eye-care spinoff from Bausch Health.

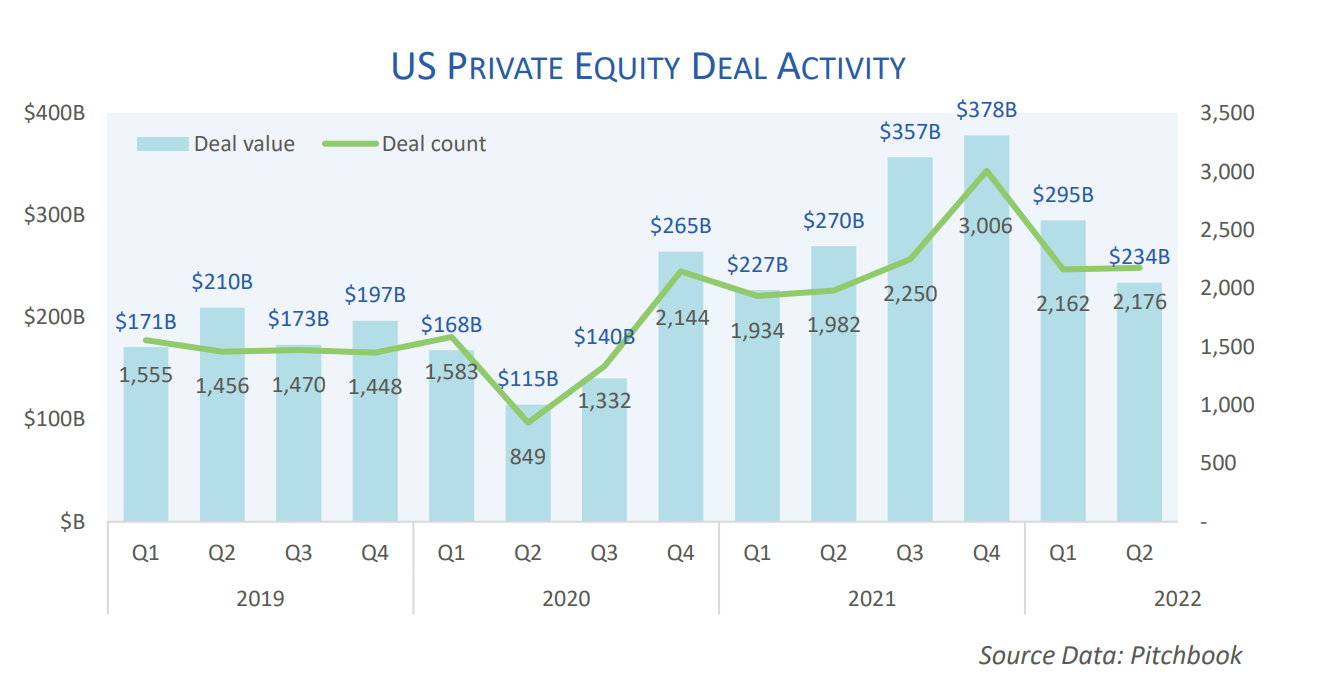

Private equity dealmaking activity would be the second line expected to feel the impact of gusty market

headwinds, namely contracting valuations, tightening debt markets, and overall volatility. However, the

lagging nature of the market due to deals that were negotiated in late 2021 and early 2022 seems to

uplift the picture for Q1, and compared to 2019 levels, the first half of the year seems to have a healthy

level of activity. Not to be fooled by the numbers, the landscape ahead is challenging, but there are valid

factors at play that are advantageous for PE deal activity. Firms are still sitting on a mountain of dry

powder, M&A deals will likely be less competitive given strategics’ reprioritization, and companies with

cash burn may prefer a buyout scenario to business-as-usual.

M&A markets had a relatively strong beginning to the year. According to EY’s research, global M&A

activity is down 27% year-over-year, but 35% above the pre-pandemic average (2015-19), highlighting

the extraordinary nature of 2021. In the US, 2022 became the year of tech mega-deals: Microsoft

announced that it will acquire the gaming giant Activision Blizzard for $69 billion, breaking a record as

the biggest tech M&A deal in history, and Broadcom’s acquisition of VMWare for $61 billion will help the

semiconductor company diversify into enterprise software. The most notorious of all, however, was

Elon Musk’s on-and-off runs at buying Twitter for $44 billion. After announcing an agreement in April,

Musk backed out of the deal in July, only to be sued by Twitter for destroying shareholder value.

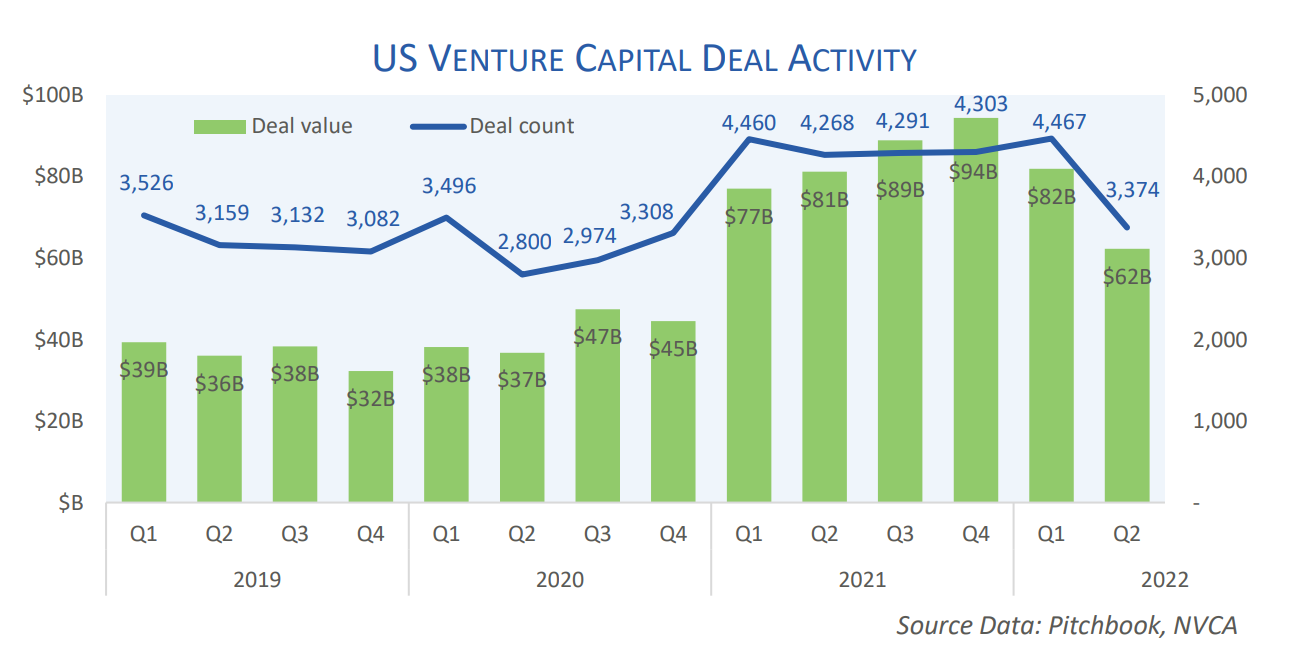

On the VC front, the trend echoes the M&A deals – while 2021 levels of activity were frothy and difficult

to maintain, there is a healthy level of deal activity relative to the pre-2021 trajectory. Per Pitchbook, 1H

2022 deal value is almost double the 2018-2020 average, and deal volume is 26% higher, while both are

down 9% and 10% against 1H 2021, respectively. It’s worth noting, that the impact of the market

correction on VC investments was felt immediately, as deal value pulled back by 24% quarter-over quarter in Q2. With the IPO exit window closed, capital becoming expensive, and economic conditions

becoming harsh, funds are preaching profitability over growth-at-all-costs, adaptability, and discipline.

Based on this confluence of factors, we expect a more measured approach prevailing over VC

investments.

In the near-term future, the market will present unparalleled risks and opportunities for everyone, and

it will likely select those with real ability and tenacity to steer their ships in raging waters.

HEALTH IT HEADLINES

Notable headlines from 2022 are outlined in the following pages on a quarterly basis. The headlines

in 2022 illustrate the significant influence that policy and regulatory intervention have on the

incentives that dictate health IT investment and innovation trends, the increasing vertical integration

across healthcare, and the expanding presence of non-traditional companies in the health IT market.

Q1 HEADLINES

Elizabeth Holmes is found guilty of defrauding Theranos’ investors

January 3: A jury found Elizabeth Holmes guilty of defrauding investors out of hundreds of millions of dollars. The verdict capped the downfall of one of Silicon Valley’s most dynamic and scandal-plagued young executives who promised to revolutionize blood testing with an innovative technology that required just a small sample of blood pricked from a patient’s finger.

Microsoft, Cleveland Clinic and Providence join coalition to innovate AI in healthcare

January 18: With healthcare increasingly placing bets on artificial intelligence, Microsoft has formed a coalition with some of the nation’s top health and life sciences organizations to build and track new AI innovations. The Artificial Intelligence Industry Innovation Coalition (AI3C) unites 9 other big names alongside Microsoft: Brookings Institution, Cleveland Clinic, Duke Health, Intermountain Healthcare, Novant Health, Plug and Play, Providence, the University of California, San Diego and UVA.

IBM sells Watson Health assets to investment firm Francisco Partners

January 21: The assets acquired by Francisco Partners include extensive and diverse data sets and products, including Health Insights, MarketScan, Clinical Development, Social Program Management, Micromedex and imaging software offerings, the company said in a press release.

ONC completes critical 21st Century Cures Act requirements, publishes the Trusted Exchange Framework and the Common Agreement for Health Information Networks

January 18: The U.S. Department of Health and Human Services (HHS) Office of the National Coordinator for Health Information Technology (ONC) and its Recognized Coordinating Entity (RCE), The Sequoia Project, Inc., announced the publication of the Trusted Exchange Framework and the Common Agreement (TEFCA). Entities will soon be able to apply and be designated as Qualified Health Information Networks (QHINs). QHINs will connect to one another and enable their participants to engage in health information exchange across the country.

DOJ sues to block UnitedHealth-Change Healthcare deal

February 24: The Department of Justice filed suit to intervene in UnitedHealth Group’s acquisition of Change Healthcare, just days shy of the company’s planned consummation date of Feb. 27. In an announcement, the DOJ said that the deal would harm competition in commercial health markets as well as the market for technology that insurers use to process claims and reduce healthcare costs.

Teladoc to partner with Amazon on Alexa-enabled virtual visits

February 28: Teladoc Health announced that it was partnering with Amazon to launch voice-activated virtual care on Alexa-supported Echo devices. According to the companies, U.S. customers around the country can connect with a Teladoc provider via audio at any time for general medical needs.

Amazon Pharmacy teams up with Blue Plans in 5 states to roll out prescription discount savings card

March 8: Amazon Pharmacy is partnering with Blue Plans in five states and Prime Therapeutics to tackle the affordability of prescription medications. The online retail giant’s pharmacy arm is rolling out a prescription discount savings card that’s available to some Blue Plans members.

Bipartisan legislation would broaden telehealth benefits for employees

March 31: The House of Representatives has drafted a bill that would provide new virtual care options for American employees. The Telehealth Benefit Expansion for Workers Act would amend HIPAA and the Affordable Care Act to allow employers to offer standalone telehealth service programs – not unlike dental and vision plans – in addition to existing health insurance plans.

Q2 HEADLINES

3M is said to consider sale of its healthcare IT division

April 26: 3M Co. is said to consider a possible divestiture of its healthcare information technology unit. The move comes after 3M (MMM) originally evaluated a sale of the unit in 2015, though it shelved the plan in 2016. The healthcare IT unit is located within 3M’s larger health group, which contributed about $9B of 3M’s 2021 revenue.

Walmart Health rolls out virtual diabetes program as retail giant moves deeper into treating chronic conditions

April 28: Walmart’s telehealth provider, MeMD, is rolling out the virtual diabetes program as a standalone service or as part of a comprehensive medical and behavioral telehealth program for enterprise customers and health plans. The retail giant collaborated with the American Diabetes Association on the virtual program, which was developed to help employees and members close gaps in diabetes management through early intervention, Walmart Health executives said.

DOJ launches investigation into Cerebral’s prescribing practices

May 7: Mental health startup Cerebral said it is under investigation by the Department of Justice (DOJ) for “possible violations” of the Controlled Substances Act. Cerebral Medical Group received a grand jury subpoena from the U.S. Attorney’s Office for the Eastern District of New York. The Controlled Substances Act regulates the distribution of potentially addictive medicines like Adderall and Xanax.

NowRx, Hyundai partner on last-mile medication delivery

May 13: Silicon Valley startup NowRx is teaming up with Hyundai Motor Group for a pilot project testing last-mile medication delivery, with an eye toward testing autonomous vehicles down the road. NowRx, a digital pharmacy that offers same-day and same-hour prescription medication delivery as well as telehealth services, plans to roll out the pilot project later this year, serving two micro-fulfillment centers in the Los Angeles area.

Pharmacy retail giant Walgreens looks to disrupt the clinical trials business

June 16: Walgreens’ healthcare ambitions continue to grow as the pharmacy retail giant expands its reach into clinical trials by leveraging its vast trove of patient data, its technology assets and its retail locations. Walgreens aims to revolutionize the antiquated clinical trials model with an eye toward using its community reach to increase patient enrollment as well as racial and ethnic diversity in sponsor-led drug development research, executives said.

New class action lawsuit claims Meta’s discreet patient data tracker was active across 664 provider websites

June 21: Facebook parent company Meta was hit with a class action lawsuit alleging the tech company has been collecting sensitive patient-status data through hospital websites in violation of the Health Insurance Portability and Accountability Act (HIPAA). The case was filed in the Northern District of California by an anonymous patient of Baltimore’s Medstar Health System on the behalf of “millions of other Americans whose medical privacy has been violated by Facebook’s Pixel tracking tool.”

Supreme Court overturns Roe v. Wade

June 24: The Supreme Court has overturned 49 years of a women’s right to an abortion in siding today with Mississippi Department of Health Officer Thomas E. Dobbs in Dobbs v. Jackson Women’s Health Organization. In the 6-3 decision, Justice Samuel Alito wrote the opinion for the majority, including Chief Justice John Roberts and Justices Neil Gorsuch, Brett Kavanaugh, Amy Coney Barrett and Clarence Thomas. Justices Stephen Breyer, Sonia Sotomayor and Elena Kagan dissented.

ABOUT HEALTHCARE GROWTH PARTNERS

Healthcare Growth Partners (HGP) is an exceptionally experienced Investment Banking & Strategic Advisory firm exclusively focused on transformational Health IT. We unlock value for our clients through our Sell-Side Advisory, Buy-Side Advisory, Capital Advisory, and Pre-Transaction Growth Strategy services, functioning as the exclusive investment banking advisor to over 130 health IT transactions representing over $4 billion in value since 2007.

Our passion for healthcare inspires us to not only create value for our clients but to also generate broad, overarching improvements to the functionality and sustainability of health. With our focus, we deliver knowledgeable, honest and customized guidance to select clients looking to execute high-value health IT, health information services, and digital health transactions. For more information, please visit https://www.hgp.com./