What You Should Know

- The Spending Boom: Healthcare now captures nearly half of all vertical AI spend, projected to hit $1.5 billion in 2025 (more than tripling from $450 million the year prior), according to the latest CB Insights State of Digital Health Q1’26 report.

- The Readiness Gap: Despite the massive investment, early AI pilots routinely fail. Less than 20% of enterprise healthcare data is currently ready for AI without substantial preparation.

- The Legacy Problem: Most healthcare data systems (like EHRs and CRMs) were built for billing, compliance, or sales tracking—not predictive modeling. This results in inconsistent data, such as mixed temperature units or non-standardized free-text diagnosis codes.

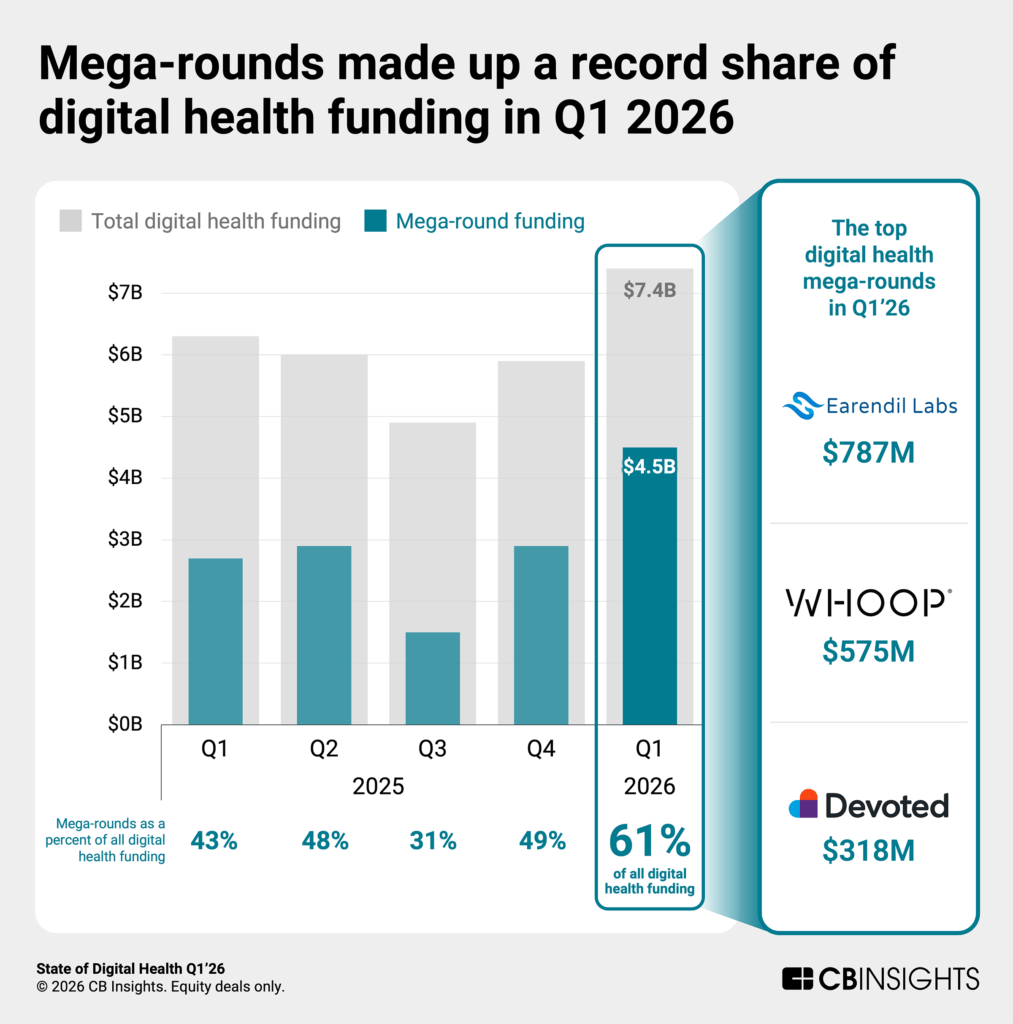

The Rise of the “Mega-Round”

Funding in Q1’26 rose to $7.4B, a sharp increase from the $5.9B seen in the previous quarter. This growth was largely concentrated in 19 mega-rounds ($100M+), which accounted for 60% of all capital raised.

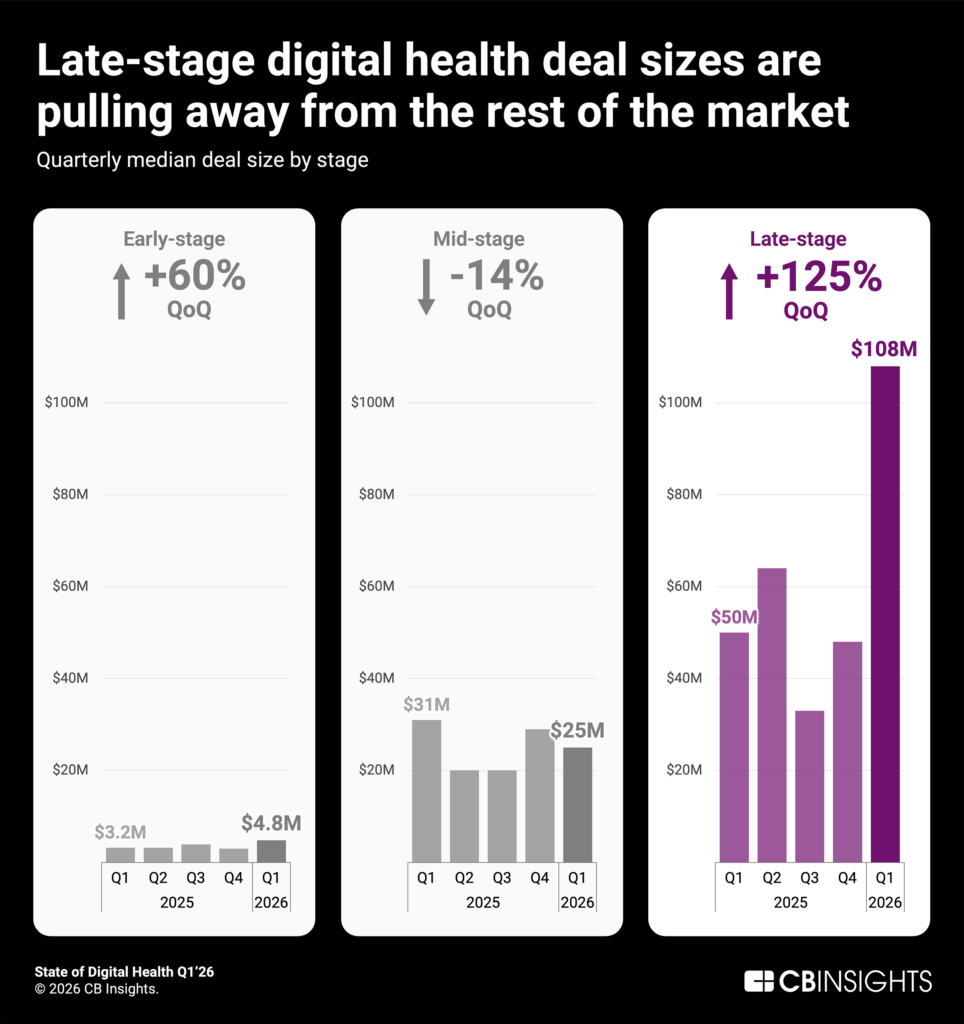

- Late-Stage Dominance: The median late-stage deal size skyrocketed to $108M, more than double the $48M median from Q4’25.

- Unicorn Rebound: Eight new unicorns were minted this quarter—the highest single-quarter count in nearly four years.

- Market Leaders: Category leaders like Devoted Health and Alan are now operating with $100M+ war chests, allowing them to remain private while expanding their distribution and acquisition capabilities.

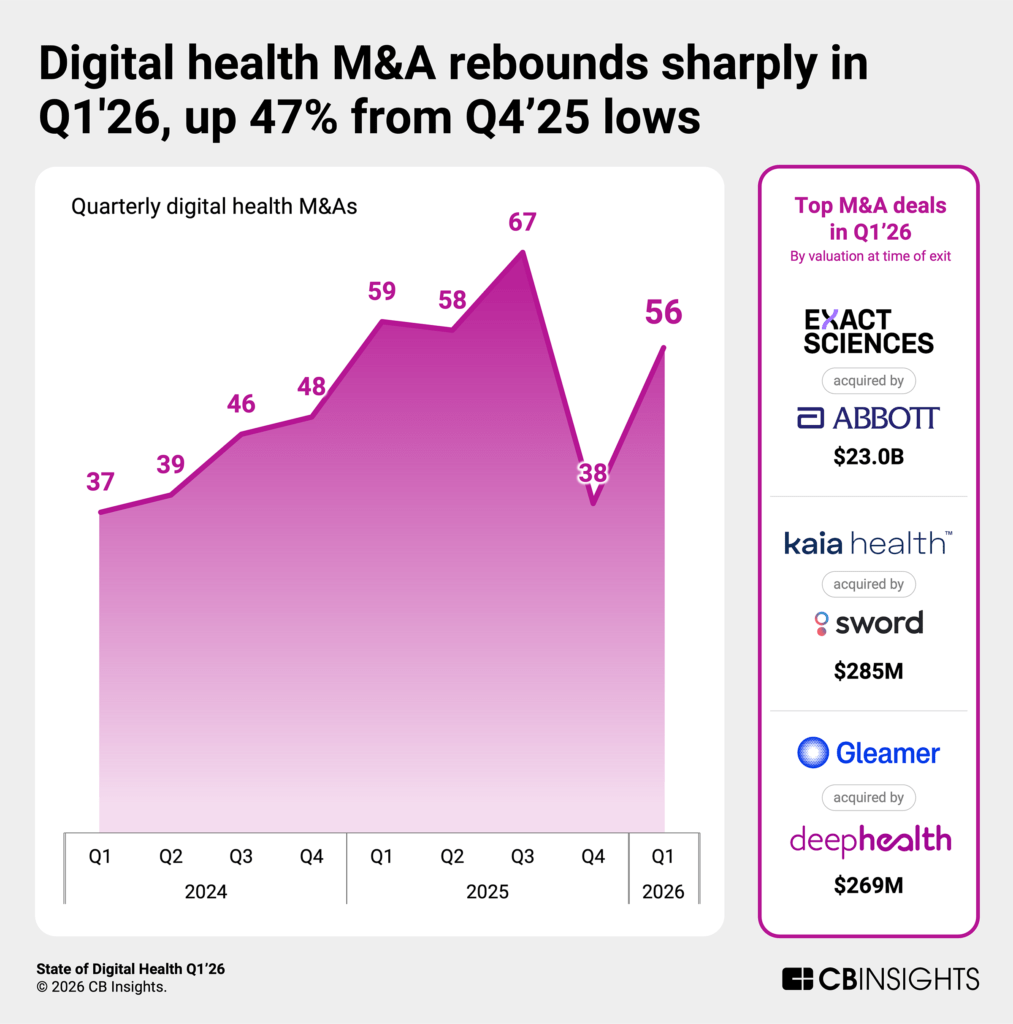

M&A Strategy: Adoption Over Approval

M&A activity jumped 47% this quarter, with 56 deals closed. The market is now strictly prioritizing commercial adoption over simple regulatory clearance.

- Abbott’s $23B Bet: In the quarter’s largest deal, Abbott acquired Exact Sciences to take its proven Cologuard screening model global.

- The Adoption Premium: DeepHealth’s $269M acquisition of Gleamer was driven by a footprint of 700+ hospital contracts. Conversely, Oxipit—despite having a world-first autonomous AI certification—saw limited value due to negligible 2024 revenue ($27.6K).

Prior Authorization: The 2027 Forcing Function

With the CMS-0057-F deadline mandating electronic prior authorization by January 2027, investment is flooding into the space.

- Pure-Play vs. Platform: Latent secured an $80M Series A as a specialized provider, while Adonis raised a $40M Series C to expand its broader revenue cycle platform.

- Strategic Partnerships: Abridge and Availity collaborated to embed these capabilities directly into clinical workflows, while Samsung and b.well are integrating portable health records into Galaxy devices to meet CMS standards.

AI Drug Discovery: Speed Meets Novelty

Pharma is committing billions to AI to compress research timelines.

- Timeline Compression: Earendil Labs raised $787M—the largest deal of the quarter—to support a deep learning platform that has already generated 40+ therapeutic programs. Takeda also committed up to $1.7B to Iambic Therapeutics, which moved a candidate to IND in just 24 months (vs. the 6-year industry average).

- Novel Modalities: Early-stage capital is targeting platforms for new drug classes, such as Proxima ($80M for molecular glues) and Vibrant Therapeutics ($61M for macromolecular therapeutics).

The Battle for Healthcare AI Talent

Headcount is growing rapidly as the market shifts from development to enterprise deployment.

- Headcount Surges: Tennr and Hippocratic AI are leading hiring in the model developer market, with Hippocratic expanding into pharma R&D following its acquisition of Grove.

- Big Tech Competition: Anthropic grew its headcount by over 200% in the last year, launching a dedicated healthcare offering in Q1’26 to rival OpenAI.

- Infrastructure Layer: Nvidia is positioning itself as the underlying compute layer for the industry, recording 6 new digital health business relationships this quarter.

For more information about the CBInsights Digital Health report, visit https://www.cbinsights.com/research/report/digital-health-trends-q1-2026/