What You Should Know

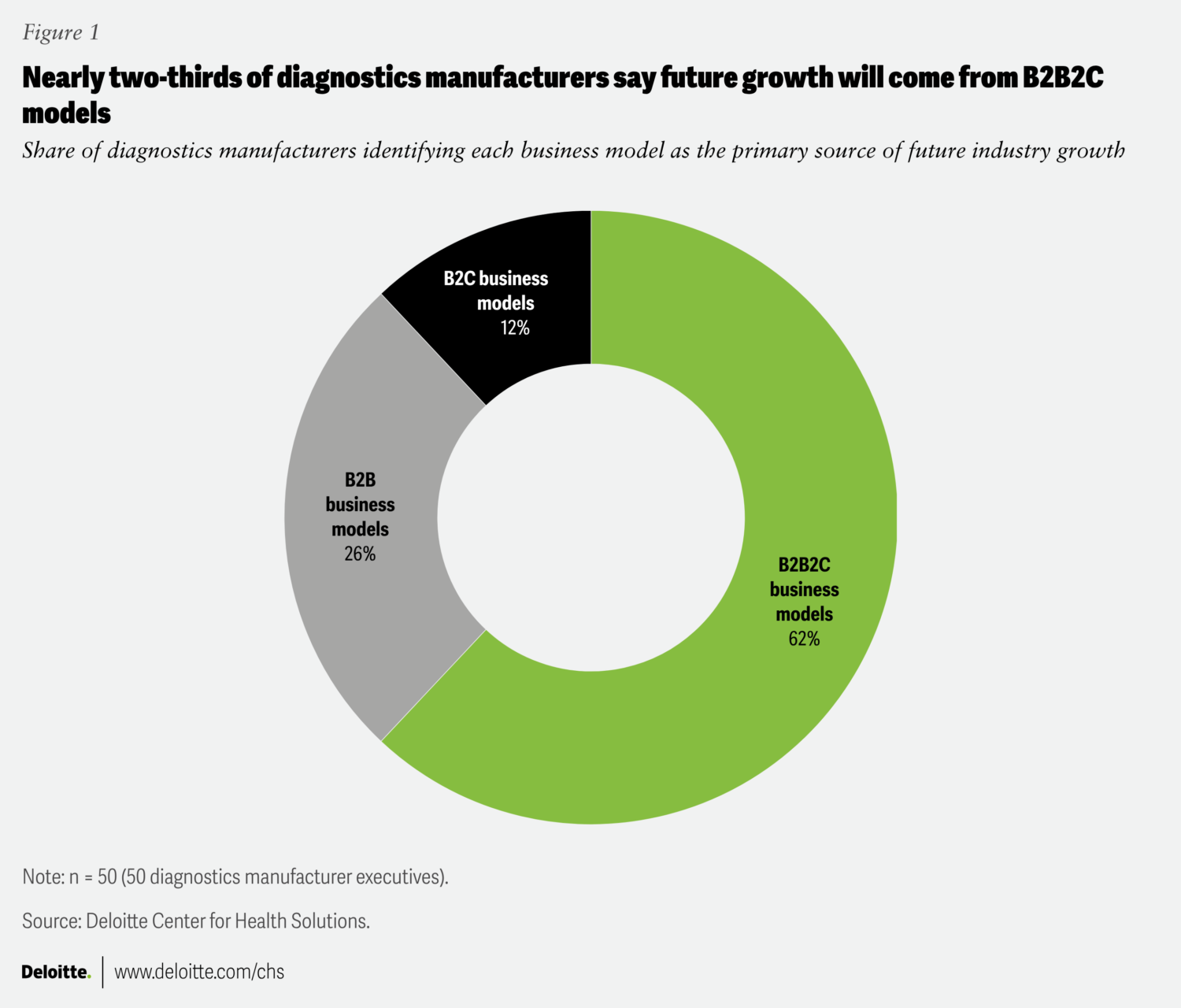

- A new survey by the Deloitte Center for Health Solutions reveals that 62% of diagnostics manufacturer executives believe future growth depends entirely on adopting a business-to-business-to-consumer (B2B2C) operational model.

- The research highlights an immediate strategic disconnect: while providers rank test ordering as their single greatest clinical friction point, manufacturers mistakenly over-index on results interpretation as the primary challenge.

- Rising consumerization is reshaping the market landscape, with 76% of provider respondents stating that consumer- and patient-initiated testing demands will fundamentally alter diagnostics over the next three years.

- Interoperability remains an acute infrastructure hurdle; 74% of healthcare providers admit that their current database systems are completely disconnected and un-integrated across the end-to-end diagnostic journey.

- To survive the expansion of home diagnostics and wearables, manufacturers must embed AI natively within EHR workflows, automate prior authorizations, and deliver highly personalized, visual data context directly to consumers.

The B2B2C Migration: Why Diagnostics Manufacturers Must Shift from Product Vendors to Workflow Partners

The global diagnostics manufacturing sector is currently navigating an aggressive, multi-directional market disruption. On the consumer front, patients are rapidly adopting sophisticated, distributed health tools—utilizing virtual healthcare portals, direct-to-consumer (DTC) self-ordered testing, digital health applications, and advanced wearable sensors to independently track, interpret, and manage their baseline biological data. Concurrently, traditional healthcare providers—encompassing independent commercial laboratories, hospital systems, and imaging facilities—are under intense operational pressure to deliver faster, highly streamlined, and deeply personalized clinical experiences or risk permanently losing market share to agile, consumer-focused tech entrants.

While these shifts point directly toward a data-driven, consumer-centric, and personalized ecosystem, legacy clinical models will not vanish overnight. Traditional healthcare providers still generate the dominant share of core revenue for diagnostics manufacturers. The pressing strategic question for corporate boards is no longer how to bypass the traditional system, but how manufacturers can actively equip their core provider customers to survive and compete in a consumer-driven marketplace.

To assess industry readiness for this transition, the Deloitte Center for Health Solutions conducted parallel surveys of 50 diagnostics manufacturer executives and 50 healthcare provider executives, supplemented by 20 in-depth interviews with industry leaders. The findings reveal a stark reality: 62% of manufacturers recognize that future growth hinges on a next-generation B2B2C blueprint. However, deep structural disconnects in stakeholder engagement, workflow integration, and consumer personalization threaten to stall this critical evolution.

Dissecting the Three Core Provider Disconnects

Before manufacturers can capture the emerging B2B2C opportunity, they must re-engineer how they interact with their primary healthcare provider customers. Deloitte’s research exposes three critical disconnects where manufacturer strategies are misaligned with localized provider realities:

- The Problem-Solving Disconnect: In the study, providers explicitly identified test ordering as the single heaviest friction point in their daily clinical pipeline. Manufacturers, conversely, focused their innovation efforts on result interpretation. To bridge this gap, forward-looking manufacturers must look past physical diagnostic kits to expand their offerings into automated software and workflow services.

- The Stakeholder Disconnect: Surveyed manufacturers stated that their primary account contacts remain hospital procurement offices and channel partners—the traditional buyers who execute contracts. Providers, however, counter that the individuals who actually command clinical adoption and long-term utilization are ordering clinicians, lab directors, and service-line leaders. Manufacturers are over-investing in procurement relationships while under-investing in the clinical stakeholders who dictate actual product adoption.

- The Engagement Disconnect: Providers heavily prioritized peer-to-peer clinical education, medical conferences, and intuitive, digital self-service web portals to research technology independently. Manufacturers, by contrast, continue to deploy high-frequency field sales teams, an outreach method that several provider interviewees described as overly frequent and lacking clinical value.

Harnessing Platform-Based AI and Interoperable Moats

The urgency to fix these engagement gaps is accelerating. 76% of provider respondents state that consumer-initiated testing demands will radically transform the diagnostics footprint over the next three years. Furthermore, 92% of providers are already actively offering or exploring patient-initiated testing pathways, compared to just 70% of manufacturers—proving that frontline clinics are absorbing the brunt of changing consumer behaviors.

As testing decentralizes into the home and retail environments, providers are becoming nodes in a distributed care network. Consumers expect visual, contextually clear results that move past raw numbers to outline actionable next steps. To help providers scale this level of personalization, manufacturers must prioritize comprehensive data and workflow integration. Currently, the tech stack is highly fragmented: 74% of providers report that their backend systems are entirely un-integrated across the end-to-end diagnostic journey.

This data isolation creates a significant entry point for platform-integrated Artificial Intelligence. Rather than deploying isolated, standalone algorithms, the competitive advantage belongs to integrated platforms that connect data across revenue cycles, automated prior authorizations, and native EHR workflows. 66% of provider executives state that personalized workflow integration will be exceptionally important over the next three to five years. Manufacturers that embed their testing infrastructure within these automated loops can capture a continuous, longitudinal view of patient health extending far beyond the clinical encounter. Those that resist this integration risk being relegated to interchangeable commodity test vendors with zero visibility into consumer behavior and no influence over future diagnostic decisions.