What You Should Know

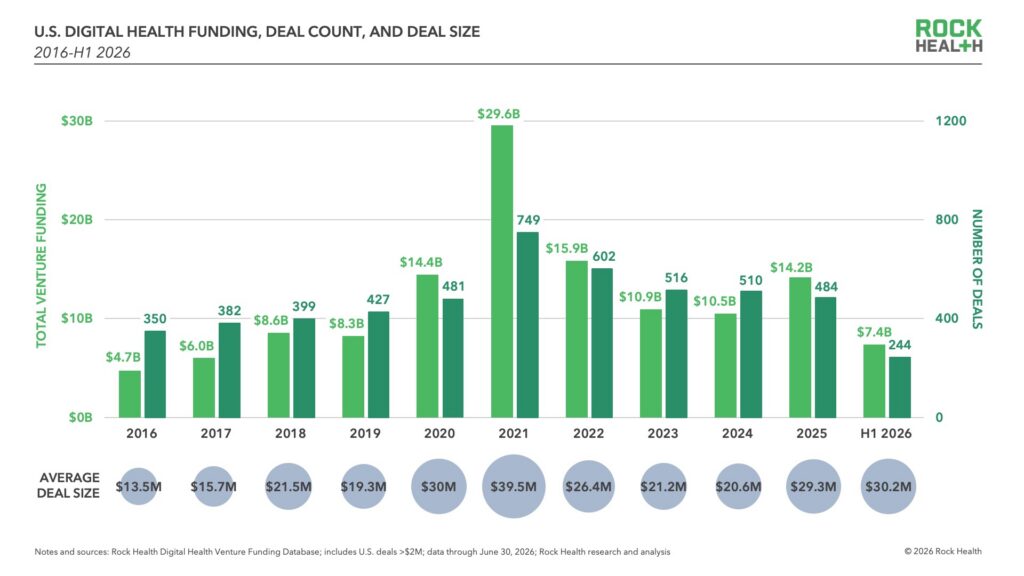

- Rock Health Capital H1 2026 Digital Health Funding Report, U.S. digital health funding reached $7.4B across 244 deals in H1 2026, outposing H1 2025 by $1B and establishing a clear multi-year recovery from the post-pandemic market resets of 2023 and 2024.

- Mega deals ($100M+) absorbed a staggering 45% of all deployed capital in H1 2026, consolidating nearly half of the market’s total funding into just 8% of finalized transactions.

- Mental health secured its position as the top-funded clinical indication for the seventh consecutive year, closely followed by weight management/obesity, which is scaling rapidly around an insatiable GLP-1 and consumer peptide ecosystem.

- As basic “AI features” become baseline expectations, sustainable advantage has shifted toward hard-to-replicate structural assets: Founder Edge, Operating Layer Scale, Hands-On Delivery (Forward-Deployed Engineers), and Compounding Network Effects.

- The digital health M&A exit field ran exceptionally hot with 115 acquisitions finalized in H1 2026, driven by intensive private equity and corporate consolidation across the Revenue Cycle Management (RCM) and metabolic layers.

The Indication Duopoly: High-Acuity Mental Health and the GLP-1 Surge

The concentration of healthcare investment capital is mapped tightly against high-volume consumer demand, with mental health and weight management/obesity anchoring the first-half clinical indication charts.

Mental Health Infrastructure Continuity

For the seventh consecutive year, mental health leads all clinical indications. To overcome the structural supply-demand mismatch between expanding patient needs and constrained clinician capacity, capital is flowing away from un-governed, direct-to-consumer chat widgets toward highly secure provider marketplaces and multi-specialty clinical layers.

Reflecting an industry-wide focus on strict safeguards and clinical oversight, institutions are backing specialized networks that pair human practitioners with automated back-end workflow routers.

The GLP-1 and Peptide Ecosystem Explosion

Driven by an insatiable global appetite for metabolic therapeutics, weight management secured the second-highest indication funding spot, anchored by three massive platform expansions: eMed ($200M), Nourish ($100M), and Midi ($100M). This clinical layer is maturing rapidly as pharmaceutical manufacturers bypass traditional distribution bottlenecks to partner directly with digital platforms for direct-to-consumer access.

Furthermore, this infrastructure is extending downstream into public coverage channels via the Medicare Bridge pilot program, which offers a $50/month GLP-1 pathway for eligible recipients.

This infrastructure maturation is simultaneously drawing investor attention to adjacent peptide categories—including wellness, longevity, and experimental age-reversal formulations—with early capitalization rounds closing for players like Superpower ($30M), Protocole ($6M), and Feel Peptides ($3M) ahead of the FDA’s late-July 2026 peptide reclassification guidelines.

Rearchitecting the Moat: The Four Rules of AI-Era Competition

Because baseline artificial intelligence features have become entirely ubiquitous across the global software market, calling an enterprise platform “AI-enabled” has lost all strategic differentiation. Incumbents like Epic are equipping health system IT divisions with low-code tools to build their own internal automated agents, raising the competitive bar for independent software vendors.

To build an unassailable commercial moat in this environment, digital health innovators must deploy four hard-to-replicate structural characteristics:

1. The Founder Edge

With software development barriers lower than ever, deep domain expertise and clinical background alignment have become mandatory to clear venture capital due diligence. Founders possessing deep clinical or administrative histories bring an authentic understanding of care team dynamics, allowing them to navigate long hospital sales cycles by directly identifying and resolving operational friction points.

2. Scaling to Own the Workflow

To survive a market crowded with single-use point solutions, late-stage startups are aggressively expanding their product pipelines to command the entire operational layer of the care continuum. Overseeing more of the backend workflow equips an automated agent with deep clinical context, enabling software networks to orchestrate complex tasks across multiple clinical departments rather than optimizing simple tasks in isolation.

3. White-Glove, Hands-On Delivery

Health system buyers maintain zero appetite for failed technology rollouts or unfulfilled return-on-investment (ROI) promises. To guarantee seamless software absorption, progressive platforms are deploying Forward-Deployed Engineers (FDEs) directly into the customer’s environment. This high-touch engineering role—originally popularized by enterprise big-data giants—co-develops custom workflows from within the client’s native architecture, a strategy heavily backed by infrastructure platforms like Commure and Qualified Health.

4. Compounding Network Effects

Sustainable value is increasingly generated by securing deep, structural integrations with clinical registries, medical societies, and industry authorities that healthcare buyers already trust. Strategic partnerships compound exponentially over time; every subsequent integration or clinical endorsement makes an enterprise application harder to replace, giving health systems a definitive reason to stay anchored inside that specific digital ecosystem.

The Corporate M&A Surge and the Public Market Divide

While the broader digital health market awaits a renewed public IPO cycle—buoyed by the highly anticipated S-1 filing of wearable ringmaker Oura at an $11 billion valuation and Whoop’s recent $575 million financing round—the exit field is currently dominated by corporate consolidation and private equity take-privates. H1 2026 witnessed 115 corporate acquisitions of digital health companies, with 71 transactions finalized in Q2 alone—marking the busiest single M&A quarter since the height of the bull market in late 2021.

This consolidation activity ran hottest across the Enterprise Revenue Cycle Management (RCM) and medical billing sectors, as health systems aggressively consolidated their backend vendors to strip out billing leaks. Prominent transactions include IKS Health’s strategic acquisition of TruBridge to extend automated RCM architectures into rural hospital communities, Innovaccer folding CaduceusHealth into its care management core, and Matt Holt’s Thoreau Group finalizing a massive $12 billion agreement to take control of RCM giant Ensemble Health.

As public markets heavily reward profitable, high-acuity data networks that clear the “Rule of 40″—evidenced by Hinge Health more than doubling its IPO price backed by a strong 23% free cash flow margin—the strategic mandate for the modern health tech executive is clear.

In an era defined by extreme clinical staffing shortages, rising uncompensated care liabilities, and strict federal focus on value-based care outcomes, the future belongs exclusively to integrated intelligence networks that can seamlessly transform raw technology fragmentation into an automated, auditable, and entirely secure system of lifelong human health.