What You Should Know:

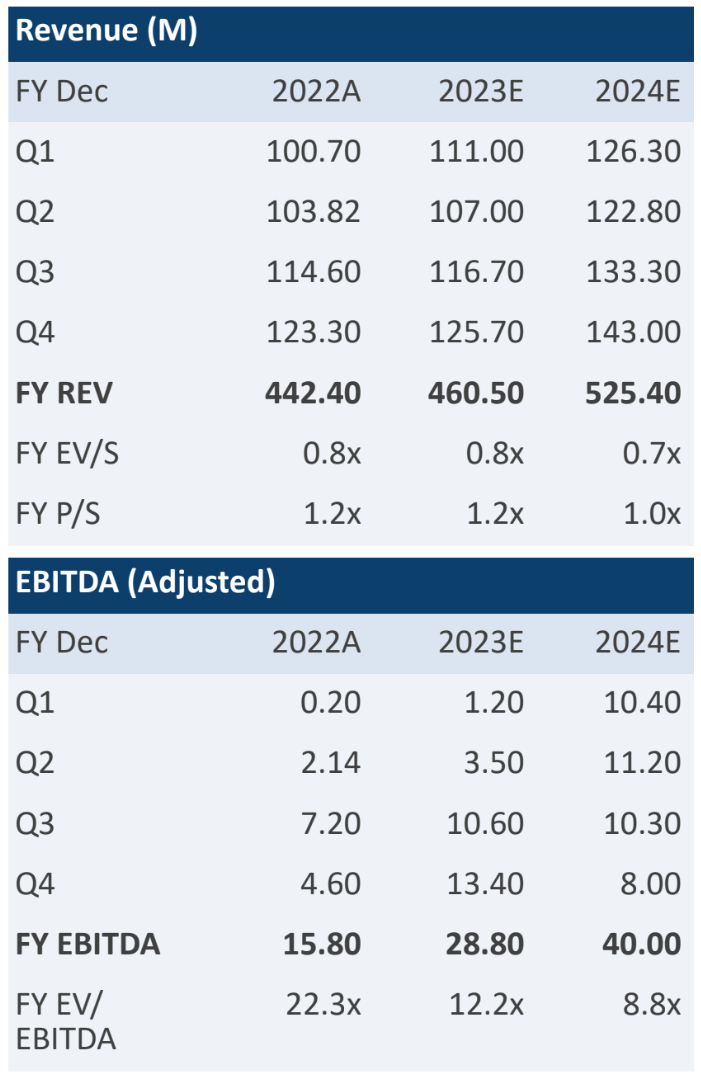

- On 5/10/23, BMO, Sharecare (SHCR) delivered what appear to be, good 1Q results. Revenue of $116.3M + 15.5% y/y, compares to BTIG / FactSet consensus of $111M / $110.9M and adjusted EBITDA of $2.1M compares to BTIG /consensus of $1.2M / $1.2M. 1Q revenue exceeded the guidance range of $111M- $113M.

- Given the top-line beat we are optimistic that revenue guidance is conservative. Management increased 2023 revenue guidance from $450-$460M to $452.5M-$460M and 2023 adjusted EBITDA guidance was affirmed at $25-$30M. Guidance for 2Q:23 looks conservative to us which is fine, we would prefer SHCR to get into the habit of consistent beat and raises. In the press report, SHCR highlighted that the company remains committed to sustainable growth, and cost optimization. It sounds like there are 12.9M lives on Enterprise and 6.5M records were processed. There was no mention of a strategic review, and it is possible that given the good 1Q performance, SHCR may decide to hold onto all of its various business units.

Good 1Q results may drive a rally, delays are not cancellations

In 1Q:23, revenue of $116.3M + 15.5% y/y, compares to BTIG / FactSet consensus of $111M / $110.9M and adjusted EBITDA of $2.1M which compares to BTIG / consensus of $1.2M /$1.2M. The midpoint of 2023 revenue guidance was notched up slightly and 2023E EBITDA guidance of $25-$30M remains intact. The most important metric in our view is revenue growth, and we view a 16% y/y increase as being good, especially compared to just +4% y/y revenue growth in 4Q:22.

As SHCR’s large new client wins are on-boarded, and as SHCR up-sells SHCR+ which carries a higher PMPM price, we would expect organic revenue growth to continue to trend favorably. In our view, it is very normal to have delays and implementation hurdles for super-sized clients like Carelon (ELV, NR) or large health plans within Carelon. Delays for a handful of very large clients can have a material impact on near-term results for any young, high-growth business, and we view lumpy revenue as being normal. Delays are not cancellations, and given that SHCR is delivering a high-quality solution, we would expect clients to purchase or come back to SHCR+.

SHCR pays attention to EBITDA and earnings

We have always liked how SHCR cares about cash flow, EBITDA and earnings. In the press report, SHCR highlighted how they are investing in their salesforce, the company is re-engineering business processes, and SHCR is implementing workforce globalization. SHCR reported 1Q:23 adjusted EBITDA of $2.1M, which was ahead of what we were expecting and full-year 2023 EBITDA guidance of $25-$30M was re-affirmed.

We do worry that earnings guidance is very much back-half weighted though this makes sense given the restructuring and re-alignment efforts that are underway, along with a potential significant ramp in revenue as more lives are added to the platform. There was no mention of a potential sale process for the Provider or Consumer Divisions, and it is very possible that SHCR may simply keep these business lines. Our view is that there is likely significant synergy, and cross-sell potential across Enterprise, Provider, and Consumer. Furthermore, while Consumer has slowed, this is reasonable and normal, given the tough ad-spend market.

About David Larsen

David Larsen, Managing Director, is a BTIG Healthcare IT and Digital Health Analyst. Prior to BTIG, David was the Founder and Senior Analyst in Healthcare IT and Digital Health at Verity Research and was a Managing Director and Senior Analyst in Healthcare IT and Distribution Research at SVB Leerink, where he spent more than a decade. He also held positions at Cowen, SunTrust Robinson Humphrey, PricewaterhouseCoopers and Care-Group Health System. David was recognized as Institutional Investor’s Rising Star in 2011, 2012 and 2013 for healthcare technology and distribution coverage. In 2015, he was recognized by the Starmine Awards as the #1 earnings predictor for healthcare providers and services. David earned an MBA in healthcare management and entrepreneurship from Boston University and a BA in economics from Boston College. He is also a member of the CFA Society of Boston.