What You Should Know:

– Since KLAS’ last report on M&A activity, there have been several notable vendor mergers and acquisitions affecting the healthcare IT landscape, and many healthcare organizations have needed to navigate the resulting disruptions.

– This report provides an update on how customer satisfaction has been affected by recent health IT M&A activity and what makes vendors more or less resilient during this type of change. This report includes 26 solutions from 20 different vendors, all of which have been affected by a merger or acquisition in the last few years.

Trends and Insights into Mergers and Acquisitions 2023

Each year, KLAS interviews thousands of healthcare professionals about the IT solutions and services their organizations use. KLAS’ standard quantitative evaluation for healthcare software is composed of 16 numeric ratings questions and 4 yes/no questions, all weighted equally. Combined, the ratings for these questions make up the overall performance score, which is measured on a 100-point scale. The questions are organized into six customer experience pillars—culture, loyalty, operations, product, relationship, and value.

Key insights from their latest report on mergers and acquisitions in 2023 are as follows:

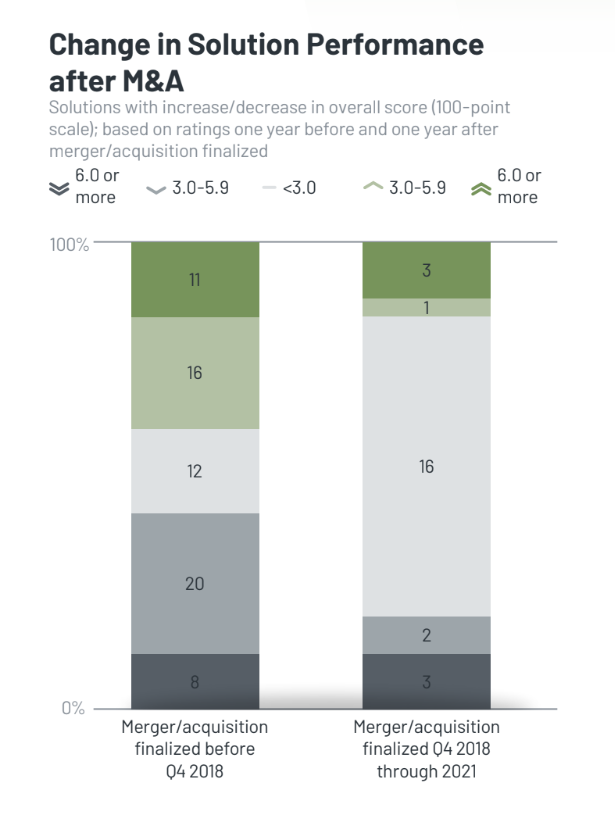

Post-M&A Disruption Has Decreased Thanks to Proactive Vendor Engagement & Communication: For 64% of measured products, there has been little to no change in satisfaction in the wake of M&A activity. Among this cohort, some clients mention that relationships and value have taken a hit. Despite this, customer satisfaction has been mostly steady as vendors’ transparent communication has helped mitigate M&A-related issues. This includes proactive outreach to client leaders before public announcements along with structures like user groups that support open lines of communication throughout the change. As long as clients see the vendor making efforts and proactively communicating, healthcare organizations seem to give their vendors more benefit of the doubt and be more resilient to changes and issues caused by M&A activity.

Strong Relationships & Culture Drive Satisfaction; When M&A Goes Poorly, Loyalty Is Undermined: Only four products in this study saw notably higher customer ratings one year after their merger or acquisition. Flywire and NextGen Healthcare each improved customer relationships through their acquisitions by focusing on client needs. ShiftWizard improved their culture ratings by keeping promises and being more proactive with customers. UKG improved in culture, loyalty, and value metrics; clients note improvements to service and support following the merger that formed UKG.

Higher-Revenue Vendors at Increased Risk for Post-M&A Performance Decline: Vendors with higher annual revenue are more likely to experience a decline in customer satisfaction following a merger or acquisition. In total, 38% of affected products from vendors with >$1B in annual revenue had a decline in customer satisfaction after their recent merger or acquisition. For companies with annual revenues between $100M and $1B, this number is 13%, and for the smallest vendors in this sample (under $100M), only 11% experienced a decline in customer satisfaction. Customers of higher-revenue vendors often share that new ownership falls short in providing effective communication, leading clients to feel they are no longer as important to the vendor. Higher-revenue vendors tend to have a large number of customers, and smaller healthcare organization clients can feel lost in the shuffle. Vendors can combat this problem by prioritizing effective communication (e.g., proactive outreach, utilizing user groups, increasing the amount of communication) before and after the merger or acquisition. In fact, several higher-revenue vendors have avoided satisfaction declines with strong communication.