As the life sciences (pharmaceuticals, biotechnology and medical sectors) M&A reaches new heights, there seems to be no end in sight for life sciences companies’ hunger for acquisitions. 94% of life sciences companies are planning to make an acquisition in the next year, with 91% of US respondents expecting these to be cross-border transactions, according to a global study of 100 senior executives at life sciences companies by global law firm Reed Smith, commissioned by Mergermarket.

The report, Life lines: Life sciences M&A and the rise of personalized medicine, explores the main drivers behind the avid pursuit for cross-border life sciences deals, the challenges faced in executing those deals, and how advances in personalized medicine may change the face of the industry.

M&A Temperature Rising

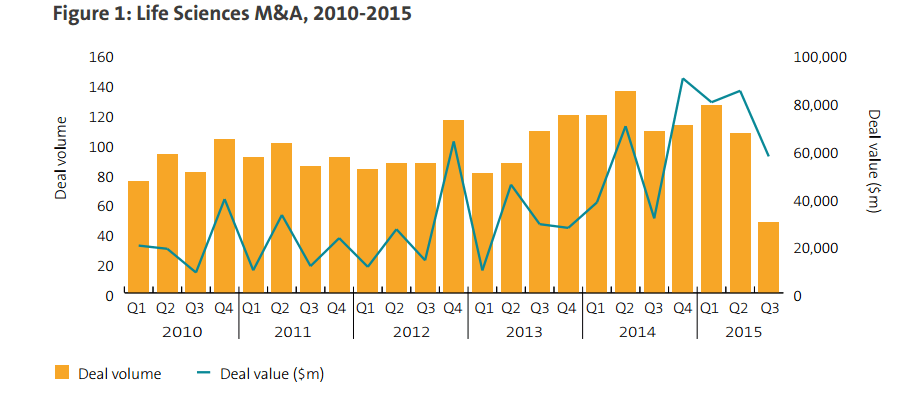

The first six months of 2015 saw $164.3B worth of deals in the life sciences sector – an increase of almost 53% on last year – while the second half of 2015 began with a burst of new transaction announcements. These included the Israeli company Teva Pharmaceutical’s $40.5B purchase of the generics division of Allergan, a US-based pharma company – the largest deal announced so far in 2015. The US saw the lion’s share of deal value in the sector, with 82 US-targeted deals announced in the first half of 2015, worth over $112B.

For many life sciences companies, acquisitions are now the preferred way to deliver the growth rates their investors have become accustomed to, with the costs and risks of developing new products in-house invariably far higher than buying a business that already is far along in the development of a breakthrough drug. As one CEO of a European pharma company observes: “It makes sense to acquire companies involved in late-stage R&D as the failure rate of early-stage R&D is so high and the mistakes are only realized when resources and time have already been utilized.”

The majority of life sciences businesses expect their acquisitions to be cross-border transactions, as they seek to capture the opportunities offered by growing markets overseas – particularly where growth in their existing markets may be slowing.

New visions

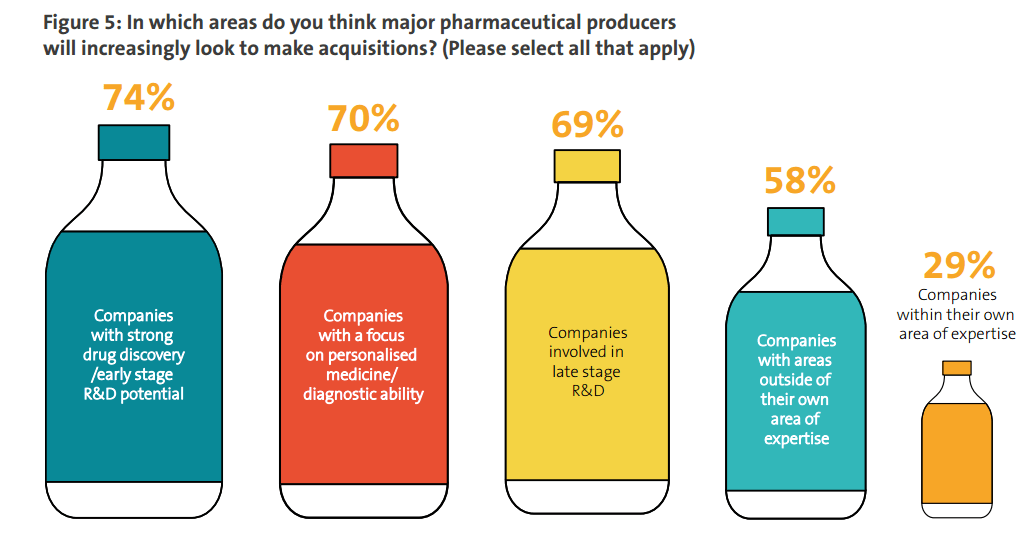

As well as deciding which geographical regions to prioritize for M&A activity, life science companies must also decide what type of company to target. . Almost three-quarters (74%) of companies hope to buy companies with products that have early-stage R&D potential, while almost as many (69%) are targeting companies active in late-stage R&D. Respondents’ interest in making acquisitions in personalized medicine (70%).

The data also illustrates that many pharmaceutical companies are keen to diversify by moving into new areas of business. More than half the companies in this research (58%) are looking to make acquisitions in areas where they do not currently have expertise. Meanwhile, less than a third (29%) are focusing on companies within their own area of expertise.

Reed Smith’s Brian Miner states the obvious reason:“It is quicker, potentially less expensive and certainly less risky to buy in this expertise than to develop it from scratch in-house.”

Over the next 12 months, US companies intend to increase investment in marketing/distribution (29% of respondents), as well as clinical trials (21%) and late-stage R&D (18%). The greatest challenges to growth are changes in healthcare policy/reimbursement (29%) and high drug development costs (24%).

Growing Role of Personalized Medicine in Life Science Companies’ Strategies

Another trend identified in the survey is the growing role of personalized medicine in life science companies’ strategies. More than two-thirds (70%) of respondents cite businesses that have a focus on personalized medicine as an area where they will increasingly look to make acquisitions.

In an era where medical practitioners are increasingly focusing on the idea of “the right drug for the right patient at the right time”, the potential prize for the producers of those drugs is a valuable one. The “one-size-fits all” approach to drug prescription feels increasingly out-of-date now that it is often possible to identify the right therapy for a patient depending on their genetic makeup and other predictive factors. “We are moving to a world where the emphasis is on gathering evidence to identify interventions that are most effective at improving health outcomes and technology is making this possible,” says the CEO of one large US pharma company.

Despite a continued focus on the development of broad application pharmaceuticals, companies recognize that personalized medicine offers the promise of higher returns even though the patient population is much smaller. “The future of medicine is to have the right medicine for the right patient and the right dose at the right time,” says Carol Loepere, Reed Smith partner in Washington D.C. and chair of Reed Smith’s Life Sciences Health Industry Group.

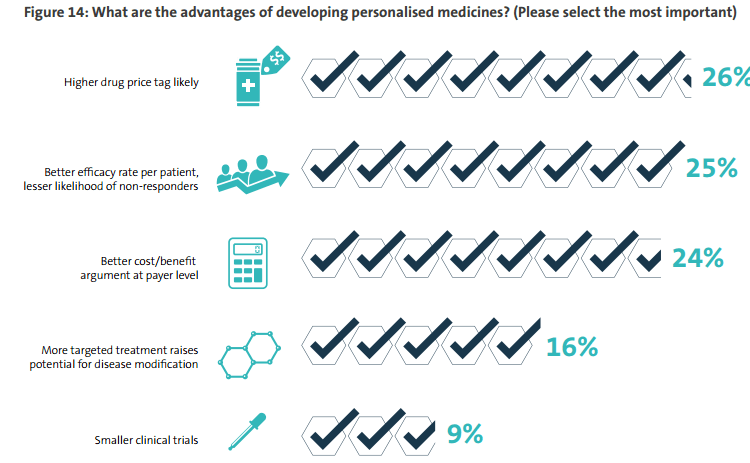

Factors Personalized Medicine Initiatives for Life Sciences Companies

The promise of personalized medicine is a happy combination of improved outcomes for many patients and an enhanced commercial performance. Most obviously, more than a quarter (26%) of life sciences companies see an opportunity to charge higher prices for more targeted drugs.

Almost as many (25%) point to the higher efficacy rate per patient of these treatments. That should encourage drug buyers to pay the higher prices quoted, since with fewer non-respondents to a treatment, its cost-benefit case improves – this is a consideration for 24% of life sciences companies.

It is relatively early days in personalized medicine, but advances are being made quickly. The UK research firm Diaceutics says 19% of therapies on the market today are targeted in some way, up from 6% in 2010, with the sector led by Roche, Johnson & Johnson and Novartis.

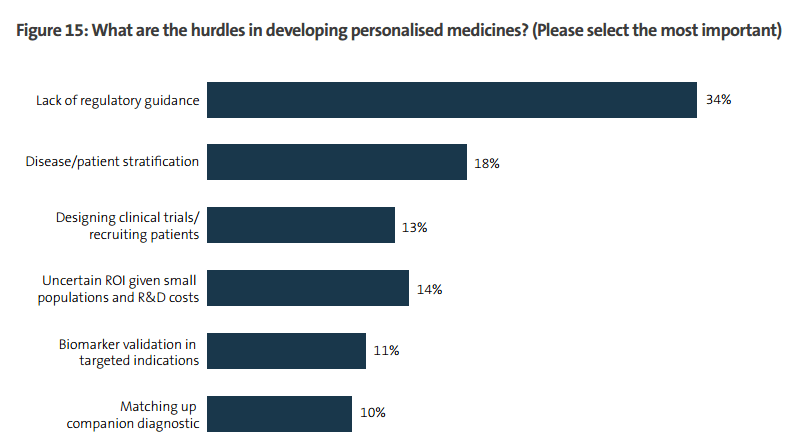

Hurdles to Personalized Medicine

Regulation is by far the biggest challenge inhibiting further advances in the development of personalized medicines. More than a third (34%) of life sciences companies complain that a lack of regulatory guidance on how they should proceed is causing them difficulties, almost twice as many as those who worry about the next most significant hurdle.

While there has undoubtedly been some progress in certain countries, the regulatory regimes that govern drug development have so far failed to keep pace with the development of personalised medicine. The US is doing best – the number of FDA-approved drugs linked with a particular biomarker has grown considerably over the past three years, to more than 80 from just over 20 – but in other markets, progress has been slower

To view the full report, please click here: http://dealdimensions.