What You Should Know

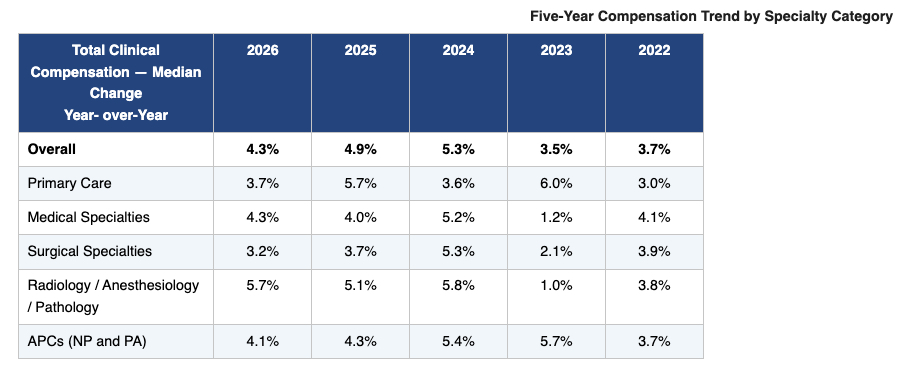

- Overall median provider compensation climbed 4.3% in 2025, driven by escalating patient demand and highly competitive labor markets for clinical talent.

- A structural bottleneck has emerged: roughly half of all provider compensation growth is being funded by increased physician output (wRVUs up 2.4%), rather than commercial or federal reimbursement gains.

- A significant shift in acuity is impacting primary care; while net patient visits dropped 2.2% (representing 60 to 90 fewer visits per doctor annually), work relative value units (wRVUs) rose 2.0% as patient complexity increased.

- The advanced practice clinician (APC) compensation gap is rapidly closing; the historic wage differential between Nurse Practitioners and Physician Assistants in medical specialties plummeted from over $7,000 to under $400.

- Facing a projected national physician shortage of up to 86,000 clinicians by 2036 and stagnant collection rates, medical groups must aggressively eliminate administrative waste to avoid systemic provider redlining and burnout.

The Productivity Trap: Why Health Systems Are Redlining Provider Output to Fund Stagnant Reimbursements

The clinical enterprise, health system financial operations, and medical group procurement landscapes have entered a period of severe structural misalignment. Over the past several years, healthcare organizations aggressively expanded their clinical capacity, optimized ambient charting tools, and deployed digital front doors to capture soaring consumer demand. Yet, this front-end volume capture has run directly into a hard macroeconomic ceiling: the widening chasm between rising provider compensation and stagnant baseline payer collections.

According to the newly released AMGA 2026 Medical Group Compensation and Productivity Survey—which aggregates data across 451 medical groups representing nearly 188,000 nationwide providers—overall total clinical compensation rose 4.3% in 2025.

While a steady compensation climb is mandatory to recruit and retain premier talent amid a looming national physician shortage, a deeper look at the underlying operational mechanics reveals an unsustainable engine.

Medical enterprises are not funding these higher salaries through improved commercial or federal reimbursement rates. Instead, health systems are balancing their books by forcing higher physician output, with overall work relative value units (wRVUs) climbing 2.4% and net patient visit volumes up 2.0%.

Relying on clinical volume expansion to offset frozen payer schedules is a strategy that is rapidly approaching its physical limits. Physicians are already pushing back against aggressive workloads by adjusting their full-time equivalent (FTE) commitments and actively seeking alternative, non-traditional care arrangements. For healthcare executive leadership teams, surviving this margin squeeze requires moving past basic volume maximization to eliminate the administrative waste that drains clinical capacity.

The Acuity Surge: Primary Care’s Silent Metamorphosis

The structural pressures impacting modern healthcare are felt most acutely within the primary care landscape. The AMGA data exposes a compelling operational pivot: primary care physician visits actually declined by 2.2% in 2025, representing roughly 60 to 90 fewer patient encounters per doctor per year.

However, despite seeing fewer physical patients in the clinic, primary care wRVUs still increased by 2.0%, driven by a significant jump in average wRVUs per visit from 1.86 to 1.94.

This metric demonstrates that primary care physicians are treating significantly higher-acuity, more complex patient panels. This change is driven by a combination of recent Evaluation and Management (E/M) coding modifications and constrained consumer access to overbooked specialists.

Because primary care physicians are managing more complex, time-intensive chronic cases, health systems must re-engineer their ambulatory workflows. Organizations need to move past traditional physician-centric charting models to deploy a highly integrated, team-based approach to patient access.

Optimizing the Advanced Practice Layer: Closing the APC Wage Gap

As healthcare groups seek sustainable pathways to extend their clinical workforce, the strategic deployment of Advanced Practice Clinicians (APCs)—specifically Nurse Practitioners (NPs) and Physician Assistants (PAs)—has emerged as a major operational priority. APC clinical compensation grew 4.1% overall in 2025, backed by a strong 3.0% increase in net wRVU productivity. This expansion underscores their vital role in preserving ambulatory access as health systems face a projected national shortage of up to 86,000 physicians by 2036.

A key operational development highlighted in the AMGA survey is the rapid closing of the historic wage gap between NPs and PAs working in identical specialty environments. Within medical specialty settings, this compensation differential plummeted from over $7,000 to under $400.

For hospital human resource executives and clinical practice managers, this wage normalization significantly simplifies the administration of APC compensation architecture. It removes a major layer of friction, allowing leadership to build cohesive, multi-disciplinary care teams that optimize patient throughput without escalating internal compliance liabilities.