What You Should Know

- The Trend: According to the new 2026 KLAS Research report, ambulatory organizations are increasingly favoring comprehensive suites (all-in-one EHR and Practice Management) over piecemeal “best-of-breed” stacks to reduce complexity and improve data flow.

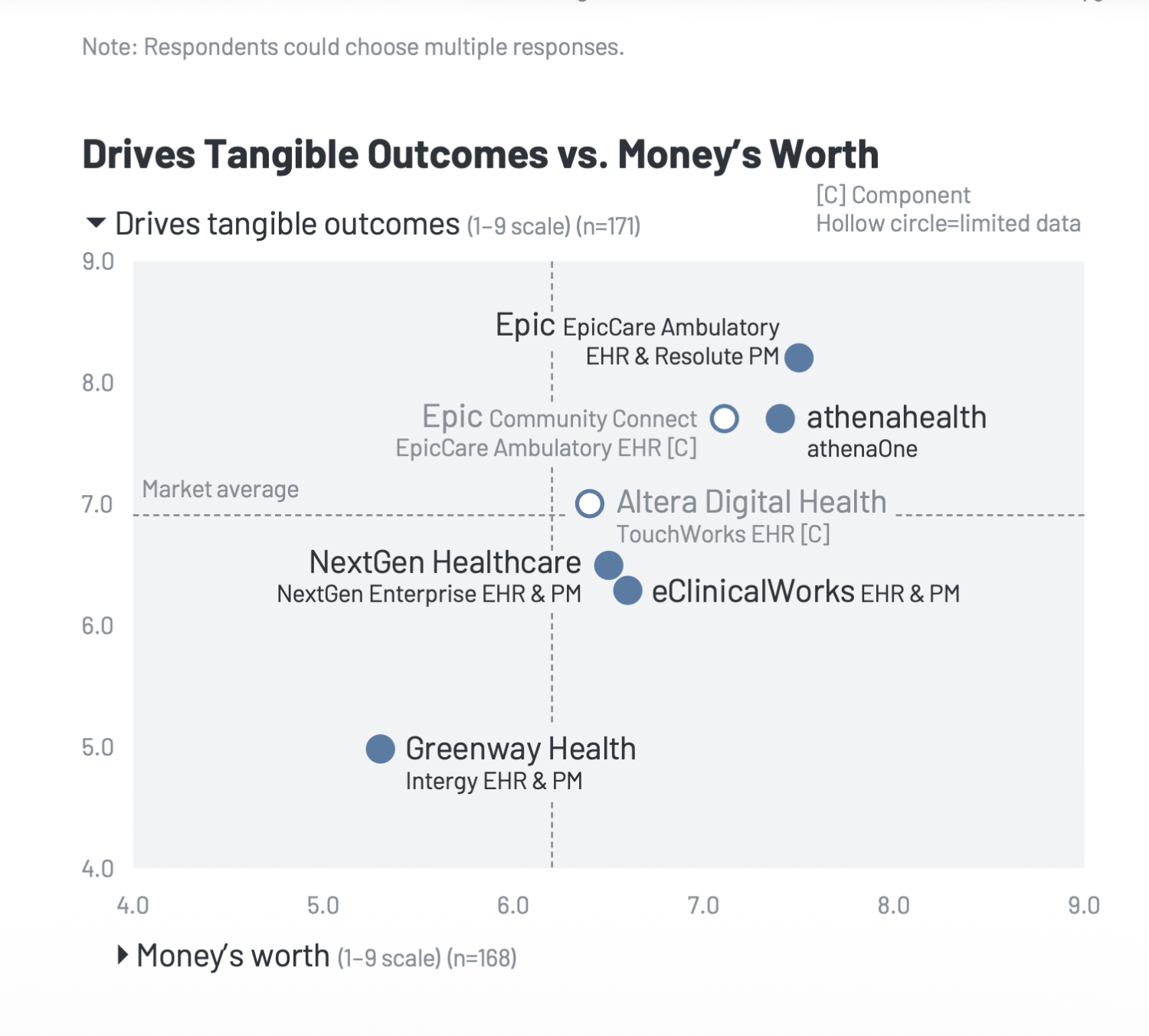

- The Leaders: Epic and athenahealth have emerged as the clear market leaders, delivering the most consistent outcomes. Their customers report high satisfaction with the “cohesive package” that supports both clinical and operational needs.

- The Gaps: Despite the push for consolidation, nearly all practices still rely on third-party tools for specific emerging technologies. Patient Engagement (66%), Ambient Speech (57%), and Patient Intake (57%) remain the top areas where core vendors fall short.

The Power of the “Single Source of Truth”

The primary driver for this consolidation is integration. Organizations report that using a single vendor for both clinical and financial workflows results in fewer manual workarounds and better visibility into patient data.

“Respondents achieve the most tangible operational and integration benefits when multiple solutions from their core EHR/PM vendor are adopted,” the report states. Beyond data flow, there is a practical IT benefit: a consolidated suite simplifies troubleshooting and eliminates the “vendor finger-pointing” that occurs when an API breaks between two different companies.

The Market Leaders: Epic vs. athenahealth

Two vendors stand out for delivering on the promise of the all-in-one suite, though they approach it differently.

- Epic: Positioned as a technology-centric enterprise platform, Epic is the go-to for large, multispecialty groups. Customers cite broad adoption of Epic tools as a key driver of success. Interestingly, Epic Community Connect customers (who use a host hospital’s instance) report the lowest reliance on third-party tools in the market, benefiting from a pre-configured, “batteries included” environment.

- athenahealth: Viewed as a services-enabled platform, athenahealth wins by bundling software with Revenue Cycle Management (RCM) services. Customers highlight the value of this “cohesive package” that scales from small practices to large enterprises.

The “Gap” Vendors

Conversely, customers of NextGen Healthcare, eClinicalWorks, and Greenway Health tell a different story. For these organizations, third-party applications are not a luxury—they are an operational necessity.

Users frequently cite “missing functionality” or “immature solutions” as reasons they are forced to look outside the core platform.

- Greenway Health: Customers frequently point to limitations in telehealth.

- NextGen Healthcare: Widespread dissatisfaction with the native patient portal drives users to third-party alternatives (though a partnership with Luma Health aims to fix this).

- Altera Digital Health: Occupies a unique/difficult spot because it no longer owns a native PM solution (it is now owned by Veradigm), forcing its EHR customers to use third-party billing tools by default.

Where the Suites Still Fail

Even for the top performers, the “all-in-one” dream has limits. The report highlights specific categories where everyone—regardless of their EHR—is still buying third-party tech.

The most glaring gaps are in consumer-facing and AI technologies:

- Patient Engagement: Used by 66% of respondents via third party.

- Ambient Speech: Used by 57% via third party.

- Patient Intake: Used by 57% via third party.

This suggests that while core clinical and financial workflows are consolidating, the “digital front door” and AI innovation layers remain a battleground for external startups.

Click here to learn more information about this KLAS report.