What You Should Know

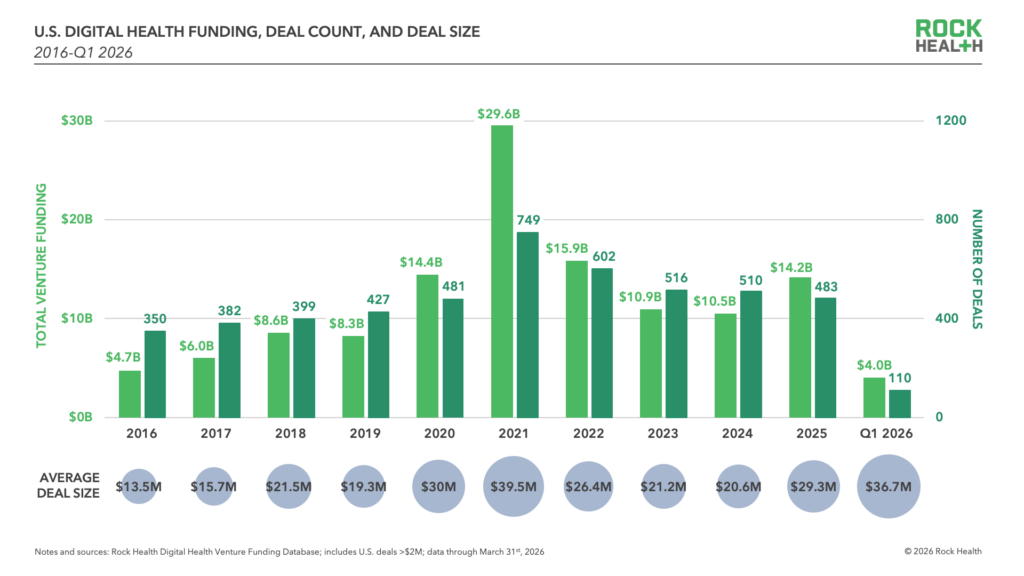

- The Top-Heavy Quarter: In the first quarter of 2025, U.S. digital health funding reached $4.0B across 110 deals with the average deal size rising to $36.7M (the highest since late 2021)., according to the latest report from Rock Health.

- The Mega-Deal Squeeze: Nearly 60% of that $4B was swallowed up by just 12 companies raising $100M+ “mega deals.” Giants like Whoop ($575M),, Verily ($300M), OpenEvidence ($250M), and Talkiatry ($212M) are pulling in nine-figure checks, leaving the rest of the startup ecosystem to battle over the remaining scraps in an increasingly volatile macroeconomic climate.

A Mixed and Patient Exit Market

The public exit window (IPOs) remains narrow, with previously flagged companies like Hinge Health and Omada Health still biding their time to ensure financial discipline before going public. The report reveals M&A activity saw a slight uptick (43 deals), heavily driven by “acquihires” as tech companies absorb talent. Meanwhile, overly ambitious roll-ups (like the attempted $32B Thoreau platform) face friction over debt and governance. For most, patience remains the dominant strategy.

AI is No Longer a Category; It’s the Operating System

In a major shift, AI-enabled startups are no longer being tracked as a distinct category because AI has become “table stakes.” Merely having AI is no longer a differentiator in healthcare. The companies that are actually raising capital right now are those executing on the grueling, unglamorous work of embedding that AI into complex clinical and administrative workflows—like integrating directly into the hospital EHR or navigating strict FDA regulatory pathways.

The Resurgence of Direct-to-Consumer (D2C)

The report notes that Investors are stepping confidently back into the D2C healthcare space. This is being driven by clearer FDA guidance, extended telehealth flexibilities, and a more activated consumer base. Additionally, consumer-facing AI platforms (like OpenAI, Anthropic, and Perplexity) are increasingly acting as the “front door” to healthcare, orchestrating health records and biometric data, which creates new distribution channels for digital health partners.

Policy is Shaping Scale and Payment Models

Policy tailwinds from 2025 are solidifying. CMMI’s ACCESS Model payment rates went live, rewarding measurable outcomes and operational efficiency at scale. With major payers adopting similar outcome-aligned frameworks, Rock Health reports the market is being pulled into a unified payment standard. Concurrently, the HHS and ONC are heavily enforcing data interoperability, pushing the industry toward true “data liquidity.”

For more information about the Rock Health Q1 2026 Digital Health Funding report, visit https://rockhealth.com/insights/q1-2026-funding-overview-capital-continues-concentrating-and-four-other-market-signals/