What You Should Know:

– The newly published AMGA 2025 Medical Group Compensation and Productivity Survey reveals substantial increases in compensation for various clinical specialties in 2024. The comprehensive analysis, encompassing data from over 184,000 providers across nearly 500 medical groups, shows a significant 4.9% compensation increase across the entire dataset, signaling a robust market for healthcare talent.

– After years of fluctuations influenced by CMS Physician Fee Schedule changes and post-COVID recovery, the survey indicates that productivity, as measured by work relative value units (wRVUs), is stabilizing across all specialties, with a modest average increase of 1.5% overall in 2024.

Compensation Growth Across Specialties

The survey highlights significant compensation increases across most specialties, with primary care leading the charge.

- Overall Compensation: 4.9% increase

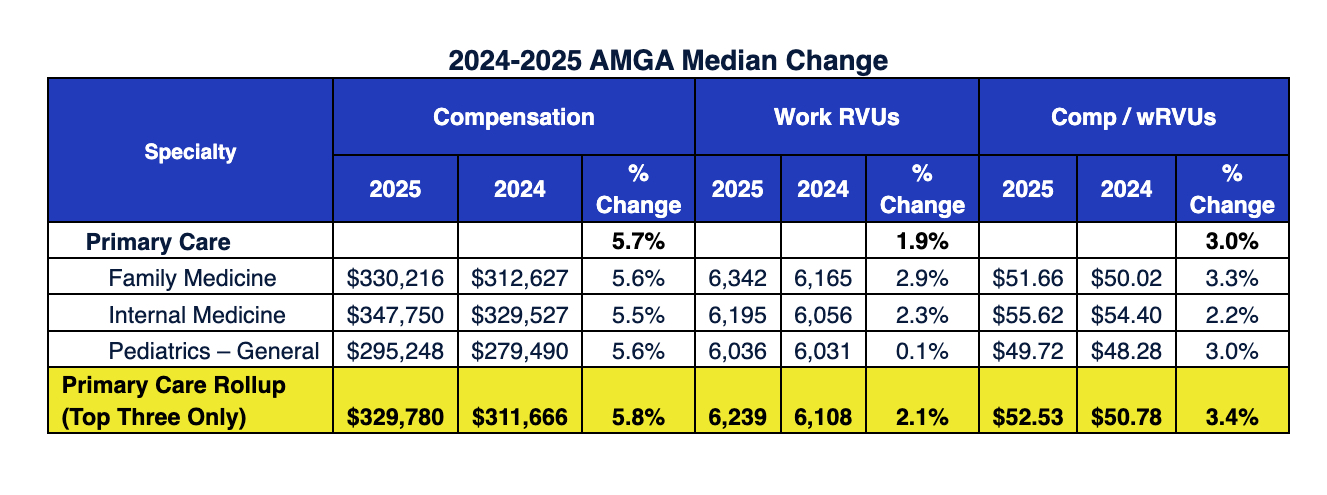

- Primary Care: 5.7% increase

- Medical Specialties: 4.0% increase

- Surgical Specialties: 3.7% increase

- Radiology, Anesthesiology, and Pathology: 5.1% increase

- Advanced Practice Clinicians (APCs): 4.3% increase

The weighted average year-over-year change in median compensation for 2025, compared to previous years, demonstrates a consistent upward trend, particularly notable in primary care which saw a significant jump from 3.6% in 2024 to 5.7% in 2025.

Productivity Stabilizes as Compensation Outpaces wRVU Growth

While compensation saw strong growth, productivity, as measured by wRVUs, showed a more modest overall increase of 1.5% in 2024. This stabilization follows years of volatility. Increases in wRVUs often correlate with a rise in patient visits, which grew by an average of 2.3% over the same period. Other factors influencing provider productivity include staffing levels, patient demand, and the increasing utilization of APCs and team-based care models.

With compensation gains outpacing productivity growth, providers experienced a 3.2% increase overall in the compensation-per-work RVU ratio. This marks the largest growth in this ratio since the COVID-19 pandemic, indicating that providers are earning more per unit of work performed. Before the pandemic, the typical annual increase in this ratio consistently ranged between +2% and +3%.

Specialty-Specific Insights

The survey provides detailed insights into various specialties:

- Primary Care: The rollup of Family Medicine, Internal Medicine, and General Pediatrics shows a 5.8% increase in median compensation to $329,780, outpacing a 2.1% increase in wRVUs, resulting in a 3.4% rise in compensation-per-wRVU.

- Medical Specialties (Excluding Hospitalists): The top three medical specialties saw a 4.9% median compensation increase against a 3.0% change in wRVUs.

- Hospitalist Specialties: Unlike other medical specialties, hospitalist compensation grew a moderate 2.5%, while productivity increased by a greater 5.8%. This led to a 1.0% decrease in the compensation-per-wRVU ratio for hospitalists, a notable contrast to other specialties. Fred Horton, president of AMGA Consulting, suggests this might indicate groups setting more specific work expectations for hospitalists, leading to higher wRVUs.

- Surgical Specialties: The top surgical specialties experienced a 3.3% compensation increase and a 1.1% wRVU increase, resulting in a 0.7% growth in compensation per wRVU.

- Advanced Practice Clinicians (APCs): Compensation for APCs increased across all specialties (4.3% overall), while overall productivity marginally decreased by 1.0%. The survey noted a “lackluster correlation between compensation and productivity for APCs,” indicating a shift in compensation philosophy as APCs comprise a larger percentage of the total provider workforce. Mike Coppola, MBA, chief operating officer of AMGA Consulting, commented that health systems and medical groups are beginning to assess their compensation approaches for APCs to ensure alignment with their plans’ philosophy, compensation plan mechanics, and care models.

Navigating a Complex Payment System

The survey also details professional net collections, which increased by 5.9% this year within primary care, medical, and surgical specialties. The past year (2024) proved challenging for medical groups, navigating a complex payment system where an initial significant decrease in the CMS conversion rate for Medicare reimbursement was partially mitigated by Congressional intervention. This forced many medical groups to explore tactics like renegotiating non-government contracts.

Future Outlook: Demand and Strategic Alignment

Physician enterprises are currently balancing provider productivity and compensation amidst various influencing factors. The 2025 AMGA survey results clearly link compensation growth to the significant shortage of providers in the industry. Medical groups are strategically balancing compensation with organizational shifts towards value-based care, experimenting with team-based care and other alternative models.

The 38th edition of the AMGA Medical Group Compensation and Productivity Survey includes data from nearly 500 medical groups, representing over 184,500 providers across almost 200 physician, advanced practice clinician, and other provider specialties.