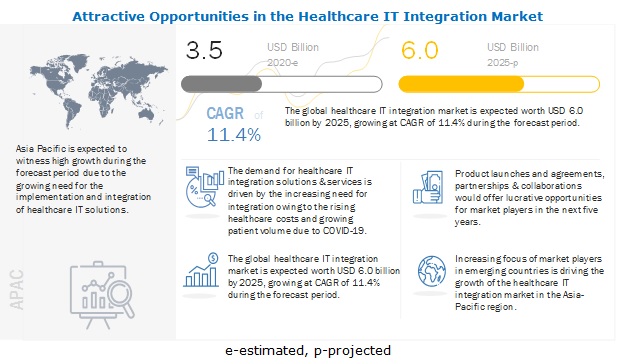

The health IT integration market is expected to grow at a CAGR of 9.6% in the forecast period, to reach $2,745.9 million by 2018 from $1,737.3 million in 2013, according to a recent report. The Markets and Markets report analyzes the global market based on products (integration/interface engines, device integration software, media integration solutions, and other integration tools), services (implementation, support and maintenance, and training), applications (hospitals, laboratories, radiology centers, clinics, device integration, HIE, and others), and geography (North America, Europe, Asia, and the Rest of the World).

Generally, hospitals and other healthcare providers have various systems for different aspects of services they provide, which are often unable to communicate with each other. In such cases, health IT integration serves as the backbone for providing a framework for the exchange, integration, sharing, and retrieval of electronic health information with advanced security. Driven by information needs, HCIT integration is increasingly being adopted by healthcare organizations to mobilize the healthcare information across or within the organization to support interoperability.

The report found growth in the healthcare IT integration market can be attributed to the rising healthcare costs, which has compelled governments in many developed countries across the world to establish cost control initiatives in their respective healthcare systems. Globally, there has been a continuous demand for Healthcare IT Integration triggered by:

- presence of strong government support and initiatives

- growing need to integrate healthcare systems

- efforts from healthcare providers to maximize their returns on investment

North America accounted for the largest share of 65% to 70% of the global HCIT integration market, followed by Europe with a share of nearly 20%. However, the Asian countries represent the fastest-growing markets. The high growth in these countries can be attributed to the increasing awareness regarding healthcare, growth in healthcare spending in emerging countries, and the presence of a large and diverse population in this region.

Key Challenges

Some of the key challenges that restrict the wider adoption of health IT integration tools within the healthcare industry include:

- Various interoperability issues

- fragmented end-users market

- high cost of implementation

The prominent leaders in the market identified in the report are InterSystems (U.S.), Corepoint Health (U.S.), Siemens AG (Germany), Orion Health (New Zealand), Infor (U.S.), Interfaceware (Canada), Enovacom (France), Cerner Corporation (U.S.), Capsule (U.S.), Accenture (Ireland), Capgemini (France), IBM Corporation (U.S.), Allscripts (U.S.), Oracle (U.S.), and AVI-SPL (U.S.).

For more information, visit http://www.marketsandmarkets.com/Market-Reports/healthcare-data-analytics-market-905.html